The Lender’s Guide to Anti-Money Laundering (AML) Compliance

With the advancement of online banking and globalisation, lenders are exposed to money laundering and financial fraud more than ever.

The latest UN findings reveal that criminals launder between $2.22 and $5.54 trillion annually, equivalent to 2% to 5% of the world’s GDP.

For Indian banks and financial institutions, the pressure is strongly felt. Both RBI and FIU-IND have tightened their grip on compliance.

This article will guide lenders in addressing the complexities of anti-money laundering compliance and the tools they can use to combat financial crimes effectively.

Why AML Compliance is Crucial for Lenders

Banks and lending institutions remain on the front lines of financial crime prevention. Anti-money laundering compliance provides their primary defence—a robust framework of checks, controls, and monitoring systems designed to spot dirty money before it enters the financial mainstream.

Without these AML safeguards, criminals can easily exploit legitimate banking channels, hampering their operational sustainability.

A compliance failure can trigger millions in fines, freeze lending operations, or revoke operating licenses entirely. Furthermore, the scandals associated with money laundering reduce client trust and damage reputation.

With digital lending now mainstream, criminals have found innovative ways to game the system, making strong AML measures not just important but critical for survival.

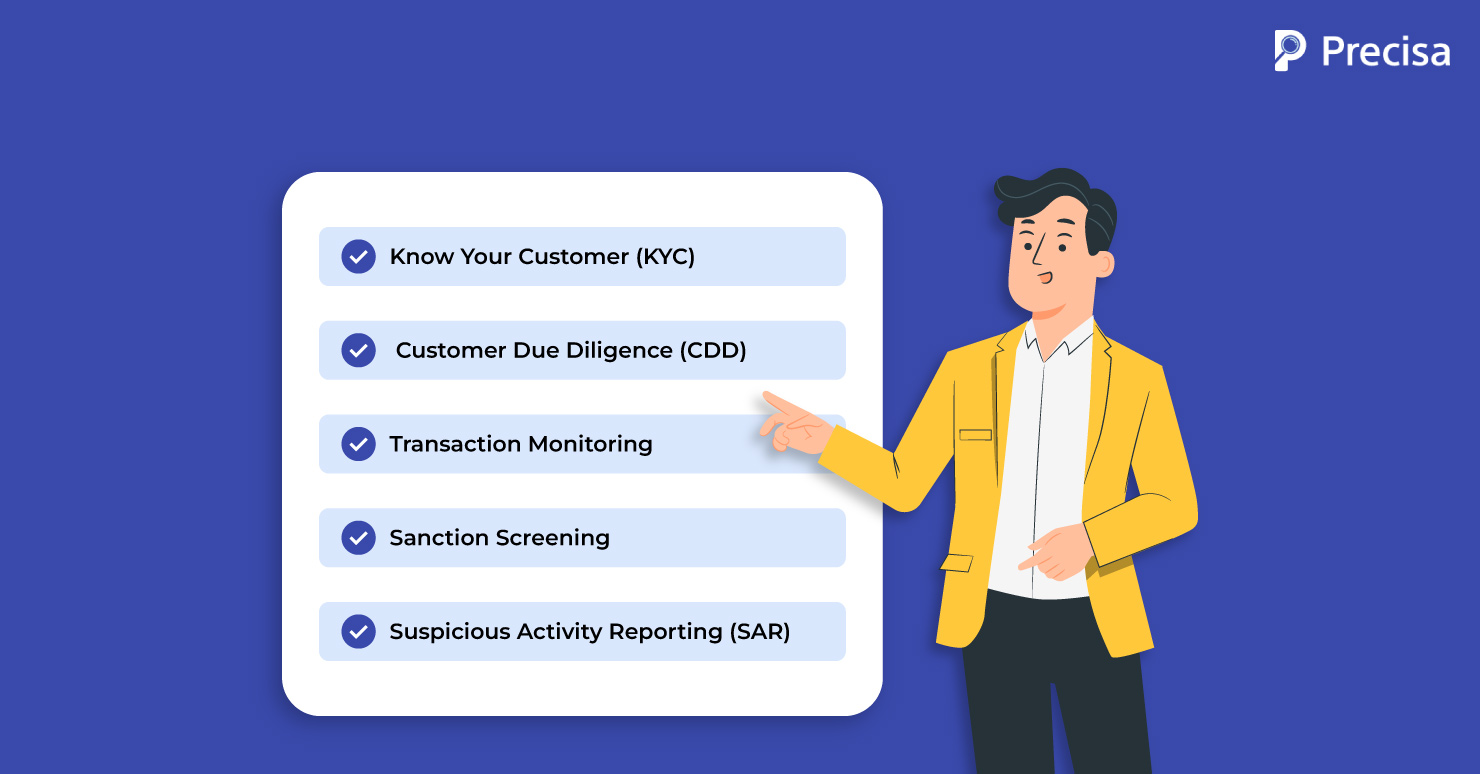

Key Components of an AML Compliance Framework

Lenders must adhere to the following key practices to ensure robust AML compliance:

1. Know Your Customer (KYC)

KYC stands as the foundation of AML compliance. Beyond initial identity verification at onboarding, lenders must track customer financial behaviour throughout the relationship.

Today’s KYC goes deeper than document checks, employing sophisticated verification methods for comprehensive profiling:

- KYC Requirements: As per PMLA and RBI regulations, KYC procedures must include identity proof, address verification, and, in many cases, biometric authentication.

- Stricter Regulations: These requirements have become more stringent with the rise of online lending.

- Data Validation: Lenders must now validate customer information against multiple government databases.

- Ongoing Surveillance: Lenders must maintain ongoing surveillance of customer profiles for any significant changes.

2. Customer Due Diligence (CDD)

CDD involves assessing customers’ risk profiles, business activities, and transaction patterns. It comprises tracking the funding sources, understanding the nature of the business relationships, and ensuring the consistency of the transactions with stated purposes.

Further, high-risk customers like politically exposed persons (PEPs), high net-worth individuals (HNWIs), and customers from high-risk countries require higher scrutiny.

This continuous monitoring helps identify unusual changes in customer behaviour or transaction patterns that may indicate money laundering activities.

3. Transaction Monitoring

Transaction monitoring in AML compliance involves sophisticated real-time systems analysing vast amounts of information.

Then, insight or patterns about the transactions are produced so as to identify the indicators of potential money laundering, such as unusual transaction volumes, structured deposits below reporting thresholds, and unexpected cross-border transfers.

The process must adapt to every customer’s unique profile, considering factors like business type, transaction history, and industry norms to minimise false positives and catch genuine suspicious activity.

4. Sanction Screening

Lenders must screen both customers and transactions against multiple global watchlists, including the UN Security Council’s Consolidated List and OFAC’s Specially Designated Nationals List. This process requires continuous updating as sanctions lists change frequently.

Modern screening systems must also account for variations in name spelling and complex ownership structures to prevent sanctioned entities from slipping through technical loopholes.

5. Suspicious Activity Reporting (SAR)

The SAR process demands both technical precision and human judgment. Lenders must file detailed reports with FIU-IND when they identify potentially suspicious activities, maintaining strict confidentiality throughout the process.

These reports must contain comprehensive information about the suspicious activity, including transaction details, reasoning for suspicion, and supporting documentation.

Setting up an AML Compliance Framework

Use the following steps for an AML compliance framework:

1. Develop a Risk-Based AML Program

Lenders must employ a risk-assessment program to:

- Understand the institution’s specific vulnerabilities.

- Establish clear policies and procedures that address identified risks while remaining flexible enough to adapt to emerging threats.

- Document all processes and decisions, from customer onboarding to reporting suspicious activity.

2. Appoint a Dedicated AML Compliance Officer (AMLCO)

The compliance officer’s responsibilities include:

- Oversee the daily compliance operations.

- Update policies as regulations change.

- Manage internal investigations.

- Ensure the institution’s AML program remains effective.

They should have direct access to senior management and the board, enabling quick decision-making on critical compliance matters.

3. Ensure Regular Training and Awareness

Employees need to understand not just the “what” but the “why” of AML procedures. This includes:

- Regular sessions on emerging money laundering techniques.

- Include case studies from real incidents.

- Provide role-specific training that addresses the unique challenges faced by different departments.

- Evaluate both theoretical knowledge and practical application abilities of employees.

4. Implement Internal Audits and Regular Reviews

A robust internal audit program serves as the final line of defence in AML compliance.

Regular reviews should examine the following:

- AML Compliance program effectiveness

- System performance metrics

- Staff adherence to procedures

- Areas needing improvement

Major Challenges in AML Compliance for Lenders

To implement an efficient AML compliance procedure, the following challenges must be addressed:

1. Keeping Pace with Evolving Regulations

The regulatory landscape is constantly changing, with new laws frequently introduced. For example, 62% of banks cite increasing regulatory expectations as their top challenge in maintaining compliance.

2. High Cost of Compliance and Cross-Border Complexities

According to recent studies, Indian financial firms spend a significant portion of their compliance budget on AML measures, with the total cost of financial crime compliance across the Asia Pacific region, including India, estimated to be around $45 billion annually, with India representing a large share due to its vast financial services market.

3. Integrating Legacy Systems with New Technologies

Many institutions rely on outdated technology that complicates compliance efforts. About 48% of banks report that insufficient AML technology is a major challenge, making integration with modern solutions difficult and costly.

4. Balancing Compliance Needs with Customer Experience

AML processes must not hinder customer experience. Research shows that 90% of bank customers may abandon an application if it takes too long. Striking a balance between thorough checks and a seamless experience is crucial.

5. Over-Reliance on Rule-Based Systems Leading to False Positives

Many AML systems generate numerous false positives due to rule-based algorithms, wasting resources and diverting attention from genuine risks. Reports indicate that 34% of compliance teams’ time is spent on writing suspicious activity reports (SARs) due to these alerts.

Key Takeaway

Effective AML compliance requires a comprehensive approach combining technology, expertise, and robust processes for lenders to maintain sustained operations.

Precisa’s Bank Statement Analysis tool provides deep insights into transaction patterns and customer behaviour, helping identify potential money laundering activities early.

On the other hand, the GSTR Analysis tool verifies business authenticity and helps detect suspicious patterns in financial flows.

Through Account Aggregator Integration, lenders can access real-time, secure financial data for enhanced due diligence. The advanced analytics platform processes this information to generate comprehensive risk assessments and automated suspicious activity alerts.

The best part? Taking the first step with Precisa is entirely free!

Sign up now to get started.