Account Aggregator Adoption in India

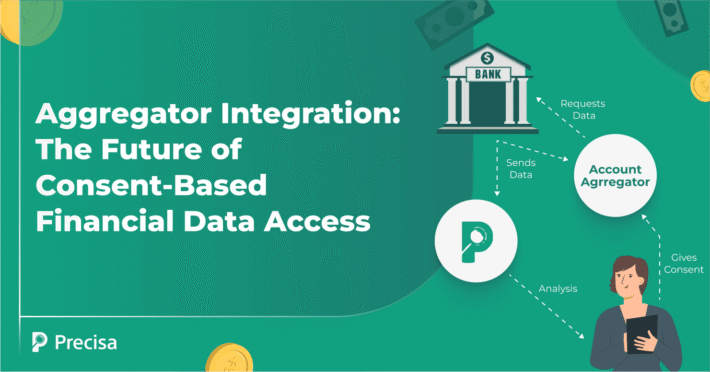

The Reserve Bank Of India introduced the Account Aggregators (AA) framework in September 2021 to facilitate access to financial data and encourage financial inclusion. An Account Aggregator collects a user’s digital financial data from one or more accounts and delivers it to the financial institution providing services like loans or insurance to the user.

The number of linked accounts touched 4.1 million by February 2023, a phenomenal growth since its launch in 2021. Finance Minister Nirmala Sitharaman, on various forums, has emphasised the benefits and opportunity account aggregation presents for Indian and global fintech companies.

In this blog, we thoroughly analyse account aggregators and why their adoption is pivotal in advancing India’s fintech goals.

Understanding The Account Aggregator Framework

An account aggregator is a Non-Banking Finance Company (NBFC) which provides services like retrieving or collecting financial data related to the financial assets of its customers. It needs a licence to start operation and performs these functions under a contract in exchange for a fee.

The network of account aggregators can be understood as a one-stop platform holding all the documents an applicant may need to apply for a loan, like past loan data, repayment history, bank and salary statements, and details of investments and assets. All this information comes directly from the financial institutions the applicant has transacted with, like the bank, insurance company, credit card issuer, mutual fund company, and more.

As the operation structure expands, the account aggregator ecosystem could become a report card of an applicant’s health where details of savings, investments, credit, insurance, pension, spending pattern and tax history are available on a single, secure dashboard. Additionally, The account aggregator framework also paves the way towards facilitating open banking in India.

Evolution of Account Aggregator Framework India

The banking system in India has witnessed numerous changes: digital banking, UPI-based payments, and more have brought more people into the formal banking framework and eased financial transactions.

However, the lending end of banking has broadly remained stagnant for the past decades, as traditional banks are often averse to risks.

The RBI’s account aggregator framework strives to remedy this and will simplify the lending and borrowing process. Therefore, what UPI did for the digital payments process, account aggregation aims to do for the loan process by reducing the steps required for a borrower to apply for a loan.

By January 2023, approximately 266 organisations were registered as financial information users (FIUs) on the account aggregator platform. 54 banks, 24 life insurers and other financial entities totalling 96 financial information providers (FIPs) are also a part of this network.

Impact of Account Aggregators on the Financial Landscape

Financial data about an individual or an organisation is usually fragmented and scattered across data repositories of FIs, government institutions and other business entities. There is no mechanism to share this data seamlessly, swiftly and safely with the permission of the user whose data is being shared.

This fragmented information is a data mine, which, if effectively optimised, can provide comprehensive, customised service delivery to users.

Here’s how account aggregators can influence:

Customer Empowerment

Despite the best efforts of the traditional banking system in India, a large segment of underbanked and underserved consumers still exists. Serving these underserved customers is challenging, especially when economic viability is considered. The availability of reliable, low-cost information often becomes a bottleneck for financial inclusivity. The account aggregator framework aims to bridge this gap.

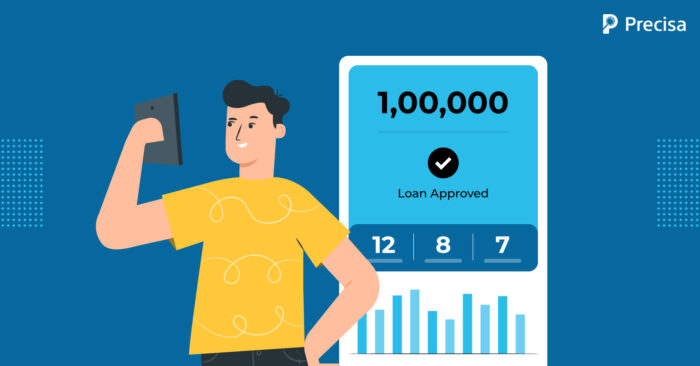

Readily available customer data will improve credit distribution and enhance the ability to provide credit to underbanked customers. Utilising this, account aggregators will enable new-to-credit customers to become creditworthy. On the other hand, lenders can analyse a host of other data points, including assets, their transactions, and repayment history, for assessing their creditworthiness.

Better financial literacy coupled with the AA framework will help customers make informed decisions and comprehend the consequences of their financial choices.

Streamline The Lending Process

The account aggregators network impacts the lending process in many positive ways.

For example, organised data sharing through account aggregators will address the current credit crunch in the Indian economy. The network can enable formal lending, with an overall positive impact on the entire economy.

It helps lenders assess the applicant’s creditworthiness more efficiently, paving the way for better lending decisions and reducing bad loans. The account aggregator system can help financial institutions expand their reach and borrower base.

Moreover, users benefit from the new framework as it simplifies the cumbersome loan application process. Borrowers can also expect better tailor-made financial solutions designed using their financial data available on the dashboard.

Benefit for MSMEs

Financial data sharing will aid in streamlining credit access for micro, small, and medium enterprises (MSMEs).

The RBI has also included the GST Network as a financial information provider under the account aggregator framework. Returns filed by MSMEs will now be a source of financial data for account aggregators.

This seamless data sharing will fast-track loan processing and also broaden the scope of financial services available to MSMEs. Lenders can base decisions on projected cash flows to cater to the credit-starved sector’s working capital requirements.

However, experts believe there is a need to move from the financial data and collateral-based credit assessment to a cash-flow-backed credit check, lending based on projected cash flows. One can fudge the account books; however, distorting GST data is impossible, giving lenders a more credible source for their lending decisions.

In Conclusion

Overall, the account aggregator platform offers a great way to speed up the loan application process, benefitting the user and the lender.

However, financial institutions may face challenges and roadblocks when integrating their systems with account aggregators. This is why the cutting-edge fintech platform Precisa and its suite of products can help you connect to account aggregators (AAs) and access financial data in real time.

To learn more about the tools that can help you contact us now!