Bank Statement & GSTR Analysis: Why Financial Analysis Requires Both

If you work in lending, financial risk assessment, or credit analysis, you’ve probably seen how many hours get swallowed by just one task: You sit down with a loan application, and suddenly half your day disappears into reviewing bank statements and GST returns. Page after page of transactions. Manual calculations. Cross-checking numbers between different documents. It used to work fine when loan volumes were smaller.

So why are both bank statement analysis and GSTR analysis important, and how do automated solutions combine them to make financial due diligence faster, smarter and safer?

Why Modern Lending Requires Both Bank Statement and GSTR Analysis

Each data source only tells part of the story. Bank statements show one thing, GST returns show another. Missing either piece means you’re making decisions with half the information you need.

Bank Statements: Where the Money Really Moves

When a business says they earn ₹10 lakhs monthly, their bank statement either backs that up or tells a completely different story.

These documents reveal behavioural patterns that predict how borrowers will handle future loan obligations. There may be a business that continuously makes overdrafts in the third week of a month or a huge cash deposit before the EMI payment dates.

Bank statements also catch fraud that’s surprisingly common in lending applications. We’ve seen cases where applicants deposit large amounts, let them sit for a few days to show healthy balances, then immediately withdraw the money. Others create fake salary credits and manipulate transaction dates to inflate their earnings.

A trained eye can spot these red flags, but automated systems catch them much faster, more consistently, and most importantly, at scale.

The key limitation is that bank statements show money movement without context.

A ₹5 lakh credit could be legitimate sales revenue, a personal loan, or money borrowed from family. Without additional information, lenders end up making decisions based on incomplete pictures.

GST Returns: The Official Ledger

GST Returns represent what businesses officially declare to tax authorities through three critical documents:

- GSTR-1 shows declared outward supplies, but doesn’t confirm if customers actually paid those invoices.

- GSTR-2A reveals input tax credits claimed, but can’t verify if those purchases were genuine business expenses.

- GSTR-3B summarises tax liability but may hide seasonal business fluctuations that bank statements would reveal. For businesses with turnover above ₹5 crores, monthly GSTR-3B filing is mandatory, while quarterly filers might manipulate timing to show inflated revenue during loan applications.

Beyond individual filings, GSTR data creates a compliance track record through filing punctuality, amendment patterns, and tax payment consistency.

This official ledger validates business legitimacy and regulatory compliance, providing crucial context about operational transparency and tax compliance behaviour. However, without bank verification, these declared revenues and expenses remain unconfirmed assumptions rather than verified financial realities.

The Critical Gap: Why One Source Isn’t Enough

Using just one data source leaves massive gaps in your risk assessment. Look at bank statements alone, and you’ll miss warning signs about tax troubles or operational issues brewing beneath the surface. Stick to GST returns only, and you have no way to confirm if those impressive sales figures actually resulted in money hitting the account.

Even when analysts manually cross-check both sources, it eats up 2-3 hours per application. Worse still, complex fraud schemes that weave through both datasets often slip past human reviewers entirely.

Automated cross-validation changes this equation completely. It spots inconsistencies and suspicious patterns that single-source reviews miss, giving lenders the full financial picture they need to make smart decisions.

How Precisa Makes Dual Analysis Effortless

Here’s how Precisa removes the friction and brings clarity to both bank statement analysis and GSTR analysis:

1. Instant Data Extraction

Using powerful OCR and AI models, Precisa extracts critical data from even the most unstructured bank statements and GSTR files in the form of PDFs, scans, and images in seconds, without a single manual input.

2. Automated Transaction Categorisation

Every inflow and outflow is sorted instantly:

- Incoming salaries

- Business income

- Payments to vendors

- Card bills

- EMIs

- Cash deposits

- One-time irregular transactions

On the GST side, it classifies B2B versus B2C sales, flags missing returns, and highlights anomalies like skipped filings or inconsistent turnover claims.

3. Cross-Validation in Real Time

Here’s where things get interesting. Precisa doesn’t just analyse bank statements and GST returns separately – it compares them directly:

- What’s declared in GSTR sales vs. what shows up in the bank account?

- Input tax credits claimed vs. payments that were genuinely made to vendors.

- Circular transaction patterns that would fly under the radar in manual reviews.

The mismatches tell the real story. Take a recent case where a business claimed ₹50 lakhs in GSTR-1 sales, but their bank statements showed only ₹35 lakhs coming in. Or consider those input tax claims that don’t line up with any vendor payments in the bank records.

When you can see both datasets side by side, these discrepancies jump out immediately. That’s the advantage of comprehensive analysis.

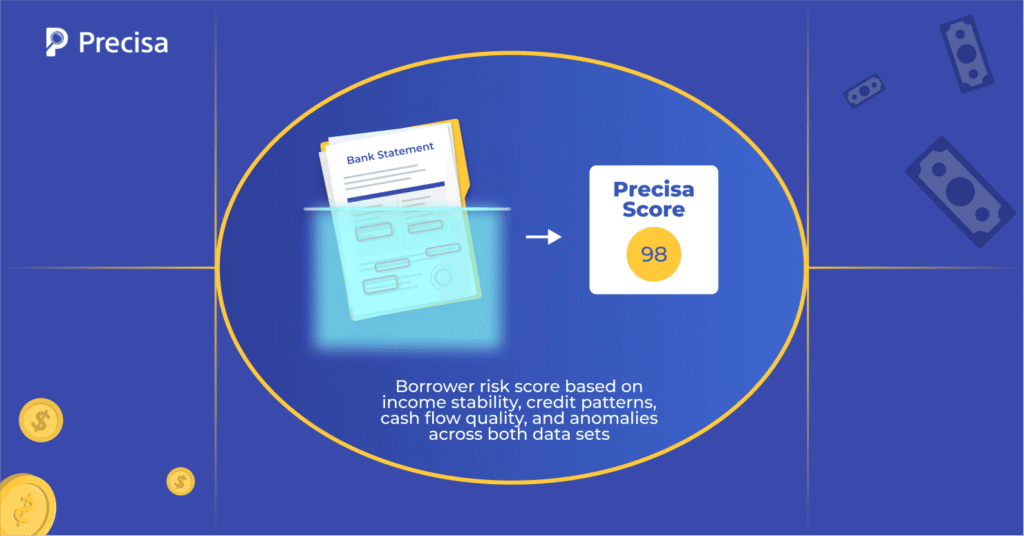

4. Scoring for Smarter Decision-Making

Precisa generates a Precisa Score, which is a unique borrower risk score based on income stability, credit patterns, cash flow quality, and anomalies across both datasets.

Lenders get a single, clear metric to assess loan repayment probability, backed by detailed transaction data whenever deeper analysis is needed.

5. Universal Format Support

Precisa covers 500+ banks, 1000+ statement formats of banks on multi-language and multi-currency platforms, including large Indian banks and multi-national institutions in 15+ countries.

Whether it’s a PDF statement from SBI, a scanned document from a cooperative bank, or a digital file from overseas operations, the AI models handle them all with 99.5% accuracy.

6. Account Aggregator Integration

Through seamless Account Aggregator integration, Precisa fetches real-time data directly from banks and GSTN servers with customer consent. This eliminates document manipulation risks, ensures data authenticity through penny-drop validation, and meets RBI compliance requirements for digital lending.

What This Means in Practice

When financial institutions switch from manual processes to automated dual analysis, the transformation goes far beyond faster processing times. Here’s what comprehensive automation delivers in real-world scenarios:

NBFCs and Banks:

Significant increases in volume handling have been reported during peak lending seasons, driven by digital transformation in NBFCs and banks. Institutions adopting combined bank statements and GSTR analysis for risk assessment have observed notable reductions in NPAs compared to traditional single-source methods.

Chartered Accountants:

Chartered Accountants save hours with automated categorisation across 100+ expense types, while deeper insights help them offer better client advice. Advanced automation helps practices handle four times more clients without expanding teams.

Government Departments:

Government departments cut investigation times from weeks to hours while generating court-ready evidence trails. Standardised reporting makes inter-agency coordination seamless.

The result isn’t just operational efficiency, but it is a fundamental shift towards data-driven decision making that reduces risk exposure while improving customer experience and regulatory compliance.

Why Automating Both Bank & GSTR Analysis is the New Normal

In today’s high-growth lending environment, relying solely on bank statements or only on GSTR filings no longer cuts it. You might get part of the truth, but never the full story. Precisa brings these together so that every cash movement is accounted for, every tax filing is cross-checked, and every risk is flagged before it becomes a liability.

The result is decisions made faster, with more confidence, and fewer surprises down the line. When comprehensive financial analysis becomes this seamless, dual automation isn’t just an advantage, it’s the new standard for responsible lending.

With RBI’s digital lending guidelines mandating comprehensive due diligence and the Account Aggregator framework enabling real-time data access, financial institutions can no longer justify incomplete analysis. Regulatory compliance now requires the depth that only combined automation can provide.

Final Takeaway

Manual analysis just can’t keep up anymore. DSAs handling hundreds of loan applications each month know this firsthand. NBFCs trying to scale their digital operations feel it too. Even forensic firms building court cases need rock-solid evidence they can defend.

The common thread? Everyone needs faster, more accurate analysis that actually meets compliance requirements. Dual automation delivers exactly that.Precisa’s combined bank statement and GSTR analysis has already transformed operations for 300+ clients across 15+ countries. Experience the difference comprehensive automation makes with a free trial covering 3 bank accounts and complete GSTR analysis capabilities.