Bank Statement Analysis: 8 Red Flags to Stay Away From During Lending

Bank statements are the most accurate record of the borrower’s income and expenses and give a fair view of their financial health. During lending, an in-depth analysis of the financial transactions of the borrower’s debits and credits over a particular period, based on their bank statements, is conducted by the lender.

The analysis provides valuable insights regarding a borrower’s recurring transactions, income and its frequency, repaying capacity, loans, balance history, obligations, etc. Bank statement analysis reveals events of non-payment or defaults, insufficient funds or bounced cheques.

Top 8 Red Flags to Look Out for During Lending

All prospective lenders ask for a copy of the applicant’s bank statement for the last three to six months. By doing so, they try to predict the chances of loan repayment.

While doing the bank statement analysis, these are some of the red flags that every lender should be careful about:

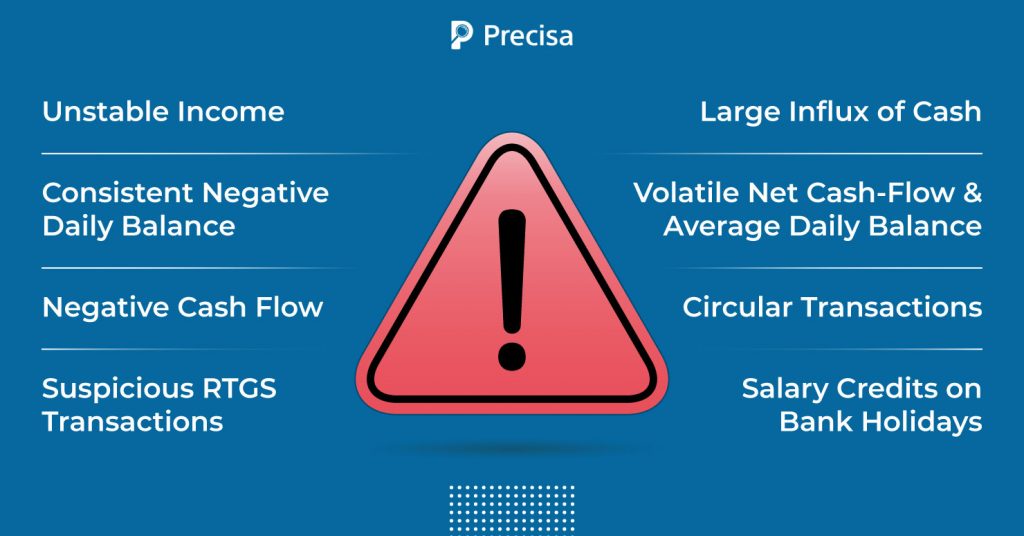

1. Unstable Income

Lenders need to know whether a borrower has enough cash in their account to not miss out on repayments in the near future. Look out for regular sources of income like paychecks or any other receipts.

In case there is any drastic change in the borrower’s income in the last few months, this needs to be clarified by them with valid reasons. For instance, an offer letter from their new job which includes their salary details would be sufficient.

2. Consistent Negative Daily Balance

If the amount remaining in the customer’s bank account at the end of the day is negative, it is undoubtedly a red flag for the lender. Also known as credit balance, this happens when the individual account holder or the company has written cheques of more value than the amount present in the bank. It could also be due to some other penalties or charges, especially those incurred by the bank.

3. Negative Cash Flow

Negative cash flow simply means the borrower has more outgoing than incoming money. They cannot cover their expenses from their income or sales alone. Instead, they need money from investments and financing to make up the difference.

Bank statement analysis can be used to spot negative cash flows easily. If the cash flow is negative, it poses a serious question over the borrower’s ability to repay the loan and should be considered a red flag.

4. Large Influx of Cash

A large sudden deposit of cash is a major red flag for lenders. For instance, the borrower might have received an enormous amount from a relative to help them cover a down payment. But they don’t have a gift letter from that relative, which explains that the deposit is a gift and not a loan that has to be repaid.

Undocumented incomes like this are a big problem for the lenders during the lending time. At times, there is an acceptable reason for a sudden increase in savings. For instance, when the borrower has had a sign-on bonus for a new job or a monetary gift from a family member. They should be asked to submit authenticated documents to show where the money has come from in such cases.

5. Volatile Net Cash-Flow and Average Daily Balance

The average daily balance shows the average amount of money held in the borrower’s account, or due on a loan, over a set period. These are used by the banks and lenders to assess the stability with income and spending of the borrower.

6. Circular Transactions

This is an artificial transaction that occurs between companies in a group,or under a single control which is mainly done to inflate the turnover of one or more of the companies.So if circular transactions are being found in a borrower’s bank statement this can be seen as a major red flag.

7. Suspicious RTGS Transactions

The Real-Time Gross Settlement (RTGS) is a fund transfer method that is done on a real-time basis without any delays. Under RTGS, there needs to be a continuous and real-time settlement of fund transfers, individually on a transaction by transaction basis.

The RBI mandates that money transactions via RTGS should be above Rs. 2,00,000. If smaller transactions are detected in the bank statement, they should be flagged as suspicious. These transactions can also be questionable when coming from the same account within a short span of time.

8. Salary Credits on Bank Holidays

On bank holidays, most transactions come to a complete halt. Companies are unlikely to process or transfer salaries on bank holidays.

So lenders need to be cautious about such salary credits reflected in the statement. This could mean a serious red flag to the lenders, and they need to have a fraud check on it.

Modern Solutions for Bank Statement Analysis

At present, most banks and other lenders rely on bank statement analysis, but it is done mostly offline. They have to employ hundreds of employees who have to parse through the data scattered across pdf statements and manually convert it to excel spreadsheets. This pdf to excel conversion is prone to errors and immensely time-consuming.

Fintech companies have come up with cutting-edge technology products for bank statement analysis. It makes the manual parsing of bank statements redundant, making the lending management and onboarding process more efficient for both borrowers and lenders.

Precisa – Smart Bank Statement Analyser

Precisa is an online financial data analytics solution wherein we democratise financial data analysis for the credit risk assessment for cash flow-based lending, wealth management, and insurance, using our software-as-a-service product that is affordable and intuitive. We help lenders and wealth managers assess the creditworthiness of their customers in minutes and at scale.

Precisa is miles ahead of today’s legacy systems when it comes to fraud detection and identifying red flags to help you make informed decisions for cash flow-based lending, insurance underwriting and financial planning.