8 Digital Lending Use Cases in India

Digital lending in India is undergoing intense activity given the massive opportunity the sector presents. According to BCG estimates, total digital retail loans could cross the $1 trillion mark in the country by 2023. With that as the backdrop, let’s look at the use cases that drive this juggernaut.

Digital Lending Models Available in India

1. Digital mortgage

The most popular and prevalent lending model, digital mortgage, digitises the entire loan process, starting with the application and ending with collection. Using digital channels optimises lending, reduces turnaround time and makes loan management more agile.

2. Invoice financing

Invoice financing meets the short-term liquidity needs of micro, small and medium-sized enterprises. Platforms that use this model offer working capital based on unpaid customer invoices.

3. Mobile loans

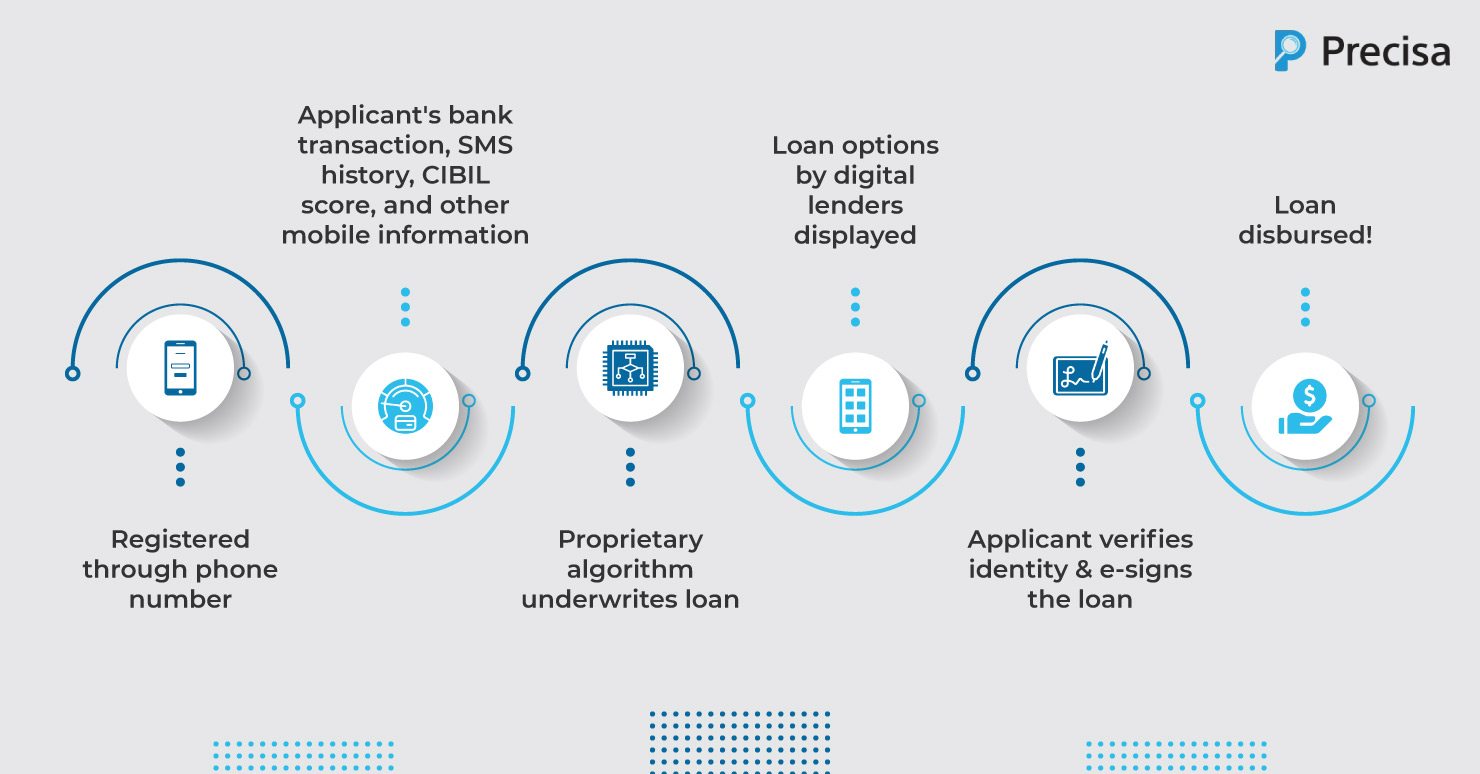

A surge in smartphone uses and the pandemic have mushroomed mobile lending in India. These unsecured loans range anywhere from INR 5000 to INR 1 lakh, are disbursed in a few short hours, and come with a short-term tenure of 30 to 90 days. The lender assesses the creditworthiness of a customer through mobile data like e-money usage and call patterns.

4. P2P lending

Peer-to-peer (P2P) lending allows a borrower to get a loan from other individuals. There is no involvement of a financial institution. A digital marketplace connects lenders with borrowers for a small registration and processing charge. The loans are available quickly and are low-cost.

5. Crowdfunding

This digital lending use case is meant for businesses hoping to raise capital through a group of investors. Platforms that rely on this model allow an investee to pitch their business, the potential of the market, and the total funds required to investors.

6. Buy now, pay later

This model is rapidly gaining traction among the end users, particularly in e-commerce platforms. The model offers small-ticket loans instantly, allowing customers to purchase items like household appliances or electronic devices. Buy Now, Pay Later (BNPL) loans often come with zero interest and can be paid in instalments or in full after a set grace period.

7. Point-of-Sale (PoS) lending

This type of digital lending forms a partnership between a merchant and a financial institute. During the point of sale, lenders extend financing options to online shoppers based on the data from the POS machine, such as transaction history, bank statements, etc.

8. Supply-chain financing

Supply chain lending ties marketplaces with financial institutions to extend financing to merchants. The marketplaces already have massive data on the merchants, and they leverage it to assess creditworthiness. Examples of this digital lending use case are Flipkart applying for an NBFC licence, Ola partnering with a bank to finance solutions for their drivers, and Cars24 acquiring an NBFC licence to enable consumer lending.

Use Cases of Digital Lending in India

Bank and Fintech partnerships

Partnerships between fintechs and banks strengthen financial inclusion. For example, a fintech company could tie up with a marketplace (think: Swiggy or ClearTrip), a data aggregator, and a bank to offer customised products to each segment. Using transaction data, the risk of a borrower can be assessed to offer small ticket unsecured loans for 30 to 60 days.

The use case enables access to capital for the underserved segment. Take, for instance, Capital Float, which partners with kirana store owners, Snapdeal, Paytm, Amazon, Yatra, etc., to offer short-term loans for amounts lower than 1 lakh against card swipes, and revolving credit.

Invoice discounting marketplace

An invoice discounting marketplace provides short-term loans to small and medium-sized enterprises. An example is KredX, which helps businesses gain working capital by discounting unpaid invoices that are raised against MNCs to a network of buyers like retail investors or NBFCs. So, once a borrower generates and raises an invoice, they list it on KredX (at a specific discount). When the invoice is paid, the full amount is directly credited to the investor.

Agri-sector digital lending

A particularly practical use case of digital lending is agri-financing, where the popular Kisan Credit Card (KCC) loans can be extended digitally. A farmer can avail of a loan using a mobile app while lenders can utilise satellite imagery, besides the usual data, to understand the land owned by the borrower and the crop grown in it.

Barring the benefit of quick and real-time disbursal of loans to buyers at minimal rates, the use case helps connect retailers with farmers for agri-inputs. A startup capitalising digital lending in the agri-sector is Bijak.

Recharge loans

A digital lending use case that is still picking up in India is recharge loans, which allow a borrower to pay utility bills in three instalments within a given period. The loan is based on the credit limit of the borrower, and it can be increased with increased usage of the app.

The model is most effective for tier-2 and tier-3 cities since the demographic has lower financial capacities. An example of this use case is True Balance.

Takeaway on digital lending

Digital lending has broken the tyranny of traditional loan processes. It’s made the sector extremely fluid, with more players using different models rising every day. For a business or a financial institute to thrive in the industry, it has become imperative to partner with a fintech company. Only with such a partnership is it possible to beat the competition and succeed.