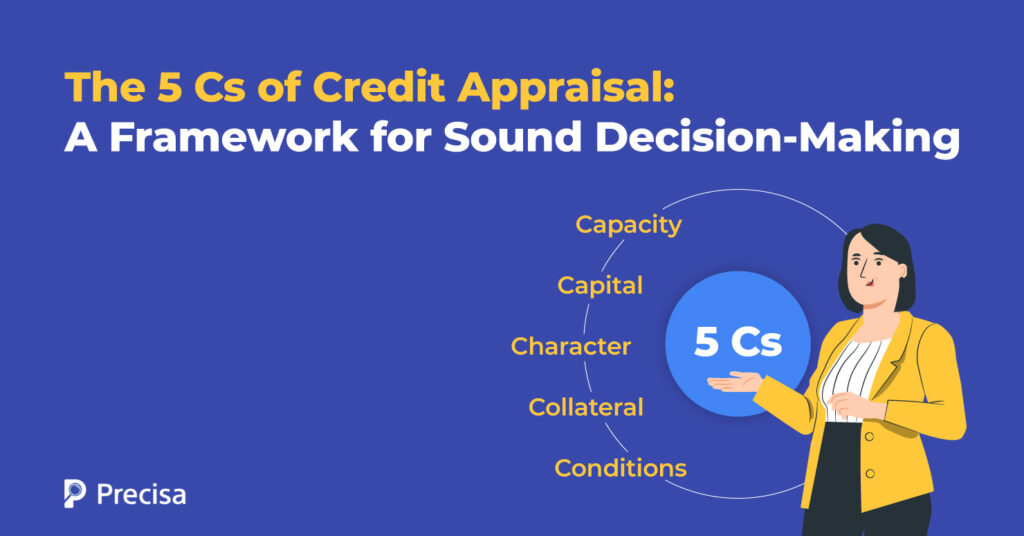

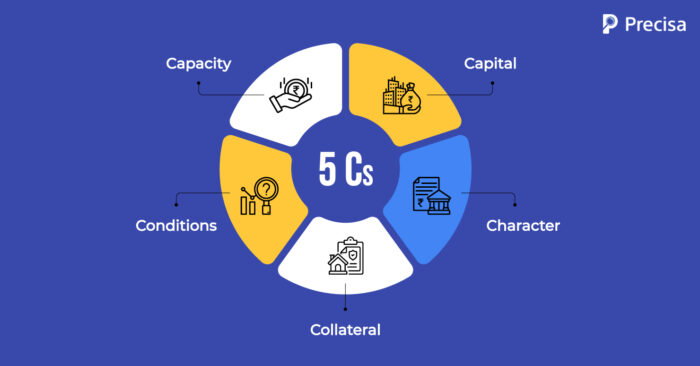

5 Cs of Credit Appraisal: A Lending Decision Framework

In a dynamic environment, several external factors — from market downturns to operational disruptions — can impact a borrower’s repayment ability. Thus, lenders must build credit appraisal systems that account for multiple risks and are robust enough to handle worst-case scenarios.

Leveraging superior bank statement analysis and financial data analytics software empowers lenders to strengthen their credit decision frameworks.

In this guide, we explore how applying the 5 Cs of credit appraisal, enhanced through technology, helps lenders make faster, smarter, and more reliable lending decisions.

What Is a Credit Appraisal?

A credit appraisal is a structured process lenders use to establish a borrower’s ability to repay a loan.

Lenders evaluate borrowers’ creditworthiness based on their financial data and credit history.

Based on the results, lenders make data-driven underwriting decisions and approve or reject the loan application. One systematic approach is to take into account the five C’s of a borrower: capacity, capital, character, collateral, and conditions.

The data analysis involved in this approach is extensive. However, using technology enables lenders to improve efficiency, accuracy, and speed.

For example, a superior tech-enabled credit appraisal software leverages several technologies to perform a comprehensive analysis of all financial information. The software uses a combination of Artificial Intelligence (AI), Machine Learning (ML), Optical Character Recognition (OCR), and Cloud Computing to drive accurate repayment predictions.

Snapshot of the 5 Cs of Credit Appraisal: Precisa’s Role

Here’s a snapshot of how cloud-based analytics platform Precisa’s comprehensive credit appraisal system brings more efficiency and accuracy to the process, involving the following stages:

Capacity

Capacity refers to a borrower’s cash flows. A healthy, consistent cash flow indicates a borrower’s ability to repay a loan based on their current revenue or income scenario. Borrowers must submit their bank statements to demonstrate proof of revenue or income to lenders.

Going forward, the terms of the loan must align with cash flows. For instance, a home loan lender typically considers a 30 to 35% debt-to-income ratio. This ratio ensures that the monthly Equated Monthly Installments (EMI) are affordable and manageable for the borrower.

Capital

As the name suggests, capital refers to a borrower’s reserve of extra cash. This cash must not be used or required for the business’s daily operations. For instance, business owners may hold financial and non-financial assets of a specific value. Financial assets refer to savings or investments, while non-financial assets stand for real estate and machinery.

An individual borrower may also have a reserve of savings or investments aside from their monthly income. The implication of having capital is this – borrowers are not dependent on their immediate income or revenues to make EMI payments. They can continue making payments even if their revenues or income are temporarily stopped.

Character

A borrower’s past behaviour can be indicative of future behaviour. Hence, lenders look at past credit patterns to understand a borrower’s attitude towards credit.

The adoption of superior credit appraisal software helps isolate all bank transactions related to EMI repayments for loans, credit card payments, or any other type of credit.

Thus, lenders can get a clear idea of debt repayment patterns, including missed payments, penalties for bounced cheques, and late fees. Credit scores and reports, additionally, offer insight into a borrower’s credit patterns and potential to demonstrate positive credit behaviour.

Collateral

Lenders typically feel more confident about giving a loan when collateral is involved.

Say an individual borrower takes out a home loan or purchases a car with an auto loan. In these cases, the home or car serves as collateral. On the other hand, a business may take out a loan to purchase real estate or machinery. In these cases, the property, machinery, and invoice value serve as collateral.

If the borrower fails to repay the loan, the lender can seize the respective collateral, such as a house, car, property, or machinery, as applicable. Thus, collateral-based loans are considered lower on the risk scale.

Conditions

The last C refers to industry-specific conditions beyond a business’s or borrower’s control. For individual borrowers, the industry refers to the borrower’s area of employment. For business borrowers, it refers to their area of business.

Lenders aim to evaluate the state of the borrower’s industry and the forecast for its overall performance in the future. Using superior credit appraisal software enables lenders to predict a borrower’s creditworthiness based on current and historical data.

Benefits of a Comprehensive Credit Appraisal

A robust credit appraisal process is essential for minimising risk and making informed lending decisions, especially in India’s diverse and rapidly evolving credit landscape.

Here’s how a comprehensive credit appraisal benefits lenders:

Improved Risk Assessment

By analysing the borrower’s financials, repayment capacity, business model, and credit history, lenders can more accurately assess creditworthiness and reduce the chance of defaults.

Better Loan Structuring

A detailed appraisal helps in customising loan terms—tenure, interest rate, and repayment schedule—to align with the borrower’s risk profile and cash flow patterns.

Regulatory Compliance

It ensures adherence to RBI guidelines and internal risk management frameworks, reducing regulatory exposure.

Data-Driven Decisions

Incorporating both traditional and alternative data—like bank statement analysis, GST filings, or cash flow projections—enhances the accuracy of credit evaluations.

Stronger Portfolio Quality

A well-executed appraisal filters out high-risk borrowers early, maintaining the health of the overall loan book.

Takeaway

Early technology investments in building a superior, systemic, and thorough credit appraisal give lenders a competitive edge. They can make data-driven decisions and accurately predict a borrower’s ability to repay a loan on time and in full.

More importantly, they can execute the process at scale and drive business growth without compromising accuracy and efficiency. This approach lays the foundation for profitable and sustainable lending operations.

Precisa’s comprehensive financial data analytics platform simplifies and accelerates this process.

Key benefits include:

- Automated bank statement analysis

- Real-time borrower scoring

- Smart dashboards delivering actionable insights

- Seamless integration with loan management systems via APIs

Request a free demo today to see how Precisa can help you build a more robust, scalable, and profitable lending operation.