4 Actions Banks Must Take To Prepare for Open Banking Wave

The banking industry is on the cusp of a significant change. Open banking, which refers to using Application Programming Interfaces (APIs) to allow third-party developers to access financial data, is set to transform banks’ operations. This new wave of open banking presents challenges and opportunities for banks.

There are four actions banks need to take to benefit from the opportunities and avoid the pitfalls. But before we dive into those actions, let’s first explore the driving forces behind open banking.

Open Banking: What’s Driving the Change?

There are a few factors that are driving open banking. Let’s take a look at each one in more detail.

- The shift in consumer behaviour: People are now more comfortable trusting third-party apps with their personal data than in the past. This shift is primarily due to the proliferation of mobile devices, the rise of social media, and the strengthening of data privacy laws.

- Regulatory changes: In Europe, the second Payment Services Directive (PSD2) aims to create a more competitive and innovative payments market. It requires banks to give third-party providers access to payment accounts. The Reserve Bank of India has proposed a similar framework for open banking.

- The rise of fintechs: There’s been increased competition from fintech startups. They use technology to provide consumers with better money-managing options. Open banking allows them to offer more innovative financial products and services.

Now that we’ve explored the factors driving open banking let’s look at the four actions banks need to take to prepare for this wave of change.

How Banks Can Prepare for Open Banking: 4 Actions to Take

Banks need to strategise to take advantage of the opportunities and mitigate the risks of open banking. Here are four actions they can take:

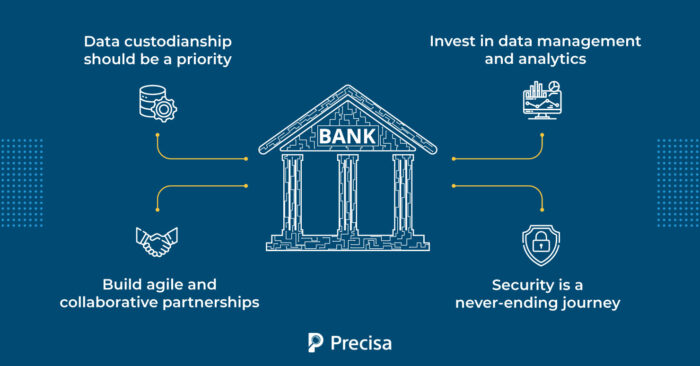

1. Data Custodianship Should Be a Priority

Data custodianship has become a hot topic in the banking industry as new technologies have emerged and developed rapidly. While banks have always been responsible for safeguarding customer data, the rise of digital banking has created new challenges.

According to the Global Banking Consumer Study, 37% of consumers trust their bank “a lot” with their data, while less than 10% trust big tech or neobanks.

Banks can leverage open banking to improve their data custodianship by implementing strong security measures and monitoring potential breaches. Banks, as current custodians of their customers’ money, are well-positioned to become custodians of their personal data.

How can banks protect their customers’ data in the age of open banking?

- Develop expertise in handling and protecting data through partnerships with technology companies.

- Implement robust security measures, such as two-factor authentication.

- Monitor for potential breaches and plan to address any incidents quickly.

- Manage customer consent and understand data privacy legislation.

2. Invest in Data Management and Analytics

Consumers in some regions are more willing to adopt open banking-powered products and services. Banks in those regions should invest in data management and analytics to better understand their customers and launch innovative products and services for their needs.

How can banks improve their data management and analytics?

- Invest in technology and partnerships that will allow for efficient data management and create a framework for data analytics.

- Provide training and resources for employees to understand and use data in decision-making.

- Create data catalogues across multiple industries that customers can opt into, allowing for personalised and targeted products and services.

3. Build Agile and Collaborative Partnerships

Open banking creates new opportunities for banks to collaborate with fintechs and other non-traditional players such as legal services firms, real estate agents, automobile dealers, travel companies, etc. Banks can leverage these partnerships to offer innovative products and stay competitive.

Forward-thinking banks must build agile partnerships that allow adaptation and growth as the industry evolves. This will help banks learn about the businesses of their strategic partners, uncover new customer segments, and build a strong ecosystem.

How can banks build agile and collaborative partnerships?

- Identify potential partners that align with the bank’s strategic goals.

- Implement a structured and shortened process for onboarding so that partners can deliver value quickly.

- Measuring partnership success using key performance indicators (KPIs) to continuously improve and adapt the partnership.

4. Security Is a Never-Ending Journey

Security is the essence of building a robust open banking ecosystem. Along with the regulatory requirements, banks must also prioritise security in every aspect of their open banking strategy. This will build consumer trust and drive the adoption of open banking initiatives.

According to a 2020 Akamai report, nearly 75% of credential abuse attacks targeted APIs in the financial services industry, indicating why consumers may be concerned about security in the open banking system. So, banks cannot afford to have a static security posture.

How can banks prioritise security in open banking?

- Implement multifactor authentication, encryption, and other measures to secure API traffic.

- Leverage behavioural biometrics and artificial intelligence to monitor for potential threats.

- Bot mitigation to safeguard open APIs against fraud, data loss, and distorted analytics.

- Continuously assess and update security protocols, staying informed about emerging threats in the industry.

Key Takeaways

Open banking presents both challenges and opportunities for the financial industry. Banks can stay ahead of the curve and thrive in this new era by taking these steps.

Building capabilities in data custodianship, data management and analytics, agile partnerships, and security will set banks up for success in the open banking wave. Once the wave washes over, the banks that have prepared will come out on top.

If you want to make your lending process more efficient, check out Precisa’s bank statement analysis tool. Our platform helps banks and lenders quickly assess borrowers’ financial health, allowing for more informed decision-making. Contact us to learn more about how we can support your open banking efforts.