Account Aggregator Integration: The Future of Consent-Based Financial Data Access

In today’s expanding digital financial ecosystem, as consumers transact, borrow, or invest online, they frequently share sensitive personal and financial data. This creates inconvenience and security risk; in this context, Account Aggregator (AA) integration emerges as a vital solution for consent-based financial data access.

With secure aggregator integration, data stays confidential. It also helps more people access financial services, gives better insights, improves tracking and analysis, and creates a better experience for customers.

The Account Aggregator (AA) framework in India was established by the Reserve Bank of India (RBI) to facilitate secure and consent-based sharing of financial data between individuals and various regulated financial institutions. AAs operate under the NBFC-AA license; the discussion below focuses on how they will shape the future financial landscape.

Account Aggregator Integration: An Overview

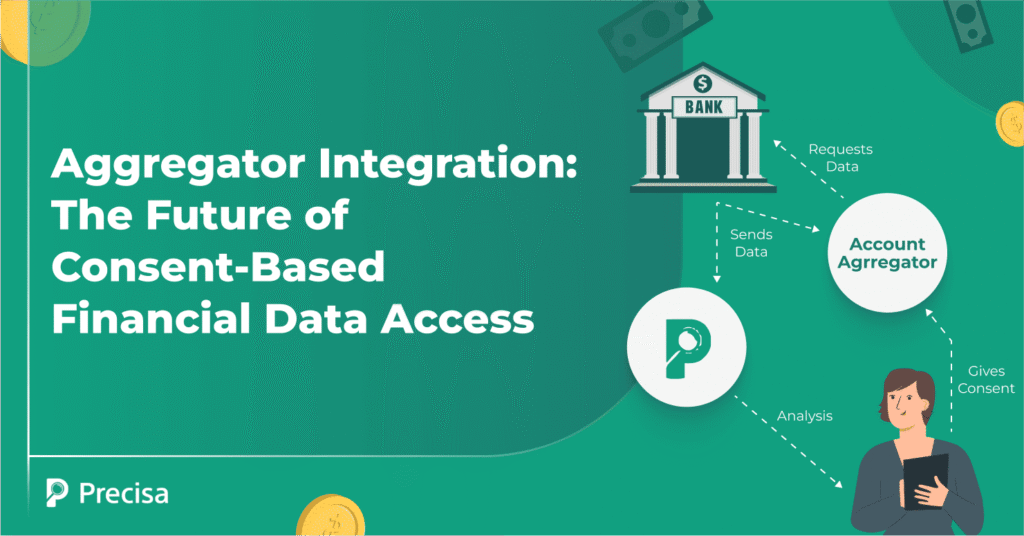

Account aggregator integration is a framework that enables a third party to consolidate, manage, and share a customer’s financial data with a financial services provider. An account aggregator, regulated by the RBI, allows individuals to securely and digitally access and transmit data from one financial institution to any other regulated entity in the AA network. The most critical aspect is the individual’s consent—no information is shared without it.

Almost 600 financial institutions participate in the AA framework, including large public and private financial institutions, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority of India, the Pension Fund Regulatory and Development Authority, and the Department of Revenue (DoR) under the Ministry of Finance, Government of India.

A few of the features of this sharing mechanism are listed below:

- The framework consists of Financial Information Providers (FIPs), like NBFCs or banks, which are the source of the information.

- The network includes the Financial Information Users (FIU), which represents the point of consumption in the form of lenders, insurance companies, etc.

- The aggregators act as intermediaries, enabling access to a consumer’s financial data with explicit consent, but cannot read or store encrypted financial data.

- The entire process is automated, making it a seamless and convenient method for the various stakeholders.

The features of account aggregator integration create a foundation of security, efficiency, and user empowerment. However, the true impact of this framework extends far beyond technical capabilities. Next, we examine why aggregator integration will shape the future of consent-based financial data access.

Why Aggregator Integration Is The Future of Consent-Based Financial Data Access?

Account aggregator integration shifts control to the individual and provides a secure, real-time, and seamless data-sharing mechanism. As consumers seek convenience, safety, and the right to decide who, when, and whether they want to share their data, account aggregator integration will shape the future in the following ways:

Transparency and Control In Data Usage

Financial institutions are repositories of data, and account aggregators empower individuals to grant and manage consent for their financial information, ensuring that sharing occurs only under the individual’s specific directives.

Encrypted data transfer between the FIPs and FIUs is guided by digital ethics and addresses concerns about information privacy and security. Emphasis is on time-bound, use-case-wise data access after obtaining the requisite permissions.

Secure APIs that integrate smoothly with existing systems ensure data sharing only happens with clear, revocable consent.

Improved User Experience

Account aggregator solutions help improve user experience in the following ways:

- Customers do not have to submit manual documents. Financial institutions can get a consolidated view of all financial information allowing faster processing and onboarding. Using Precisa’s integration solution does away with the need for physical submission of documents and facilitates secure, swift, and seamless data sharing.

- Direct and real-time data sharing reduces the turnaround time and paperwork.

- FIs can offer customised solutions based on real-time, permissioned data — such as spending habits, income trends, or financial goals.

Robust Decision Making

Decision-making improves with access to transaction data, financial patterns, and history from verified and varied sources. Bank statement analysis or GSTR analysis helps lenders assess the liquidity position and credit health of the applicant, helping them assess risks better and improve the quality of their portfolios.

Precisa’s Bank Statement Analysis tool analyses transactional patterns, spots irregularities and cheque returns, helping lenders reduce the chances of fraud and defaults.

Promotes Financial Inclusion

Many people can’t access formal credit or financial services because they lack the right documents or history. Lenders can use alternative data, like mobile payments or utility bills, for robust risk analysis and decision making. They can offer loans to the underserved segments also. Account aggregators help share this data, making sure more people get the financial services they need.

How Account Aggregators Will Facilitate Open Finance

The evolution of open banking has been facilitated by the account aggregators framework. The Indian open banking market generated a revenue of USD 1,595.4 million in 2024 and is expected to reach USD 8,254.0 million by 2030. It is expected to grow at a CAGR of 31.8% from 2025 to 2030.

Account aggregators will help move from open banking to open finance by creating a consent-based network for sharing all types of financial data, not just banking details.

Open banking focuses on sharing data between banks and third-party providers, enabling faster loan processing and improved financial management. Open finance requires data sharing across a broader range of financial sectors, including insurance, pensions, and investments, in addition to banking.

This change lets third-party providers offer more personalised services beyond banking, helping to build a more complete financial system in the following ways:

- For example, fintechs can offer personalised financial solutions after getting a holistic view of a customer’s finances.

- Or insurers can assess risk better and customise policies based on deeper, real-time customer insights.

To Sum It Up

Account aggregator integration lets users decide who sees their financial data and why. Sharing information is now fast, secure, and does not require endless paperwork. This means quicker loan approvals, tailored financial advice, and complete data privacy. It helps create a more secure, financially inclusive, and efficient financial ecosystem for businesses and customers.

Secure account aggregator integration is a crucial and strategic decision that can influence operational efficiency, customer experience, regulatory compliance, and long-term competitiveness.

Precisa offers solutions for account aggregator integration with your existing systems with a few simple steps, and gives your team a smooth, fast and secure user experience.

Request a free demo today!