Fintech-Bank Collaborations: A Necessity For Digital Banking

Banking, one of the world’s oldest industries, has been around for nearly 4000 years. From the earliest recorded temple loans in ancient Babylon, which date back to 2000 BCE, to the most recent technology-enabled services, such as open banking and Banking as a Service (BaaS), it has consistently played a systemic role in the development of the economy. Technology is transforming banking in unprecedented ways, both as a financial activity and in terms of service delivery.

Fintech, as the name implies, combines technological capabilities with financial services to create new products and delivery channels and improve overall customer experience.

While some see fintech firms as competitors to banks, this is not always the case. Banking is a financial activity fundamental to the economy’s functioning, and Fintech firms are innovating banking functions to cater to the evolving demands of a tech-savvy clientele.

In this scenario, rather than competing, it is preferable for these two entities to collaborate and reciprocate to advance digital banking.

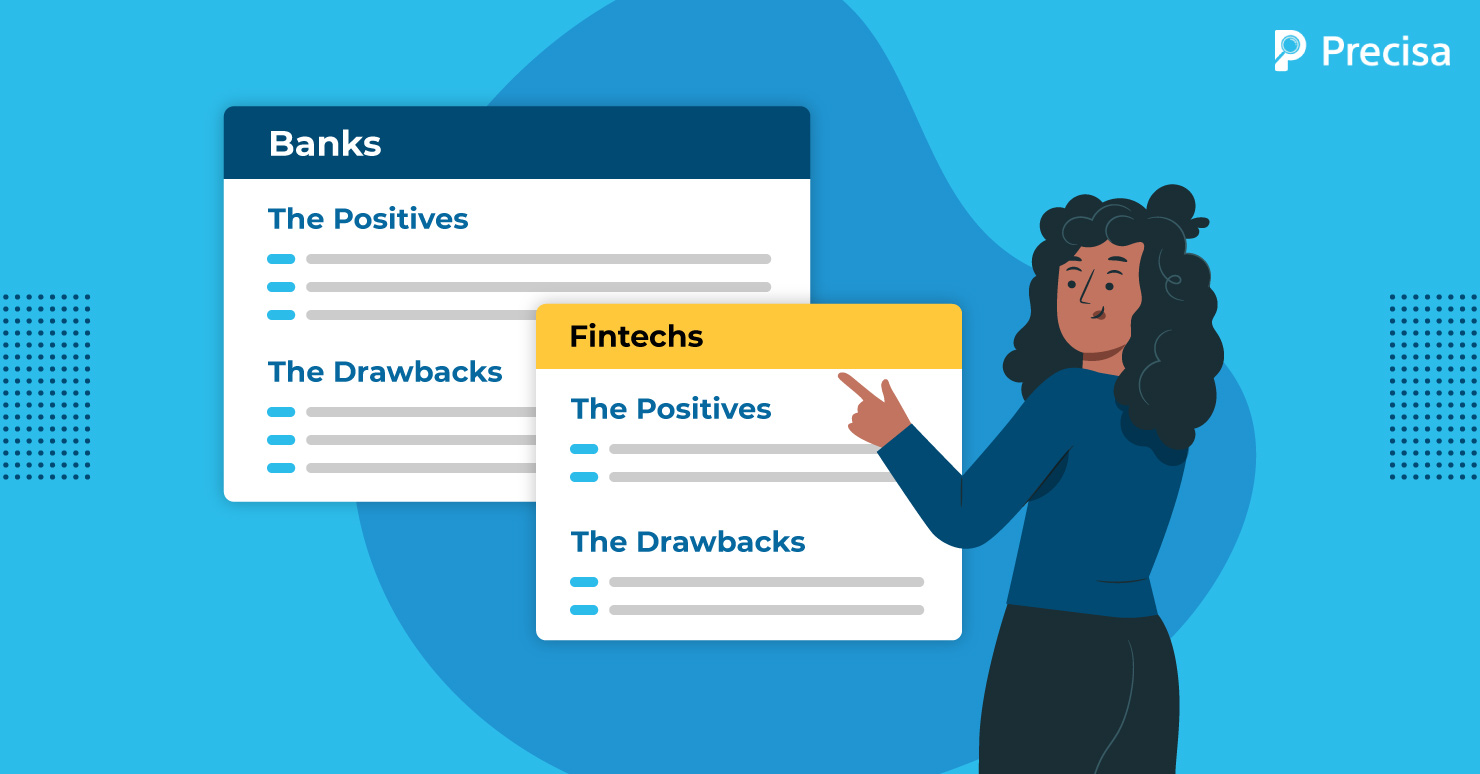

Evaluating the Competitive Strengths and Weaknesses of Banks and Fintech Firms

Assessing their strengths and weaknesses will help us better understand the benefits of bank-fintech collaboration.

Here are some relevant aspects laid side by side for comparative analysis:

The Positives:

| Banks | Fintechs |

| A strong customer base built on the public’s trust earned over many years of service. | Have more agility, better customer outreach, and can respond to service requests more quickly |

| Ability to operate in a highly regulated environment | Regulations are less strict and still evolving |

| Extensive industry expertise | No burden of legacy technologies |

| Multiple services under a single roof | Streamlined service offerings and provides better access to customers |

The Drawbacks:

| Bank | Fintech |

| Products and services lack innovation | Weak brand equity compared to banks |

| Slow in adoption and personalisation of technology | Frequently struggle to establish a strong client base |

| Low risk tolerance, especially concerning lending to MSMEs | The absence of stringent regulations raises the risk of operations. |

The Significance of Bank-Fintech Partnerships

The relationship between banks and fintechs today is both competitive and collaborative.

Both have a place in the financial ecosystem; one cannot exist without the other. Fintechs, to be sure, have a competitive advantage and have more technological relevance than banks at present.

But incumbent banks are so economically important that they cannot be pushed out of the picture by their lean and digitally adept counterparts in a single day.

Customers want end-to-end consistency and personalised services delivered seamlessly. Digital banking effectively accomplishes this expectation. Therefore, banks need to leverage digital technology to improve efficiency, scalability, and agility. Partnering with fintechs, banks can benefit from fintechs’ ability to adapt to new technologies.

On the other hand, for fintech companies, cooperation with banks provides them access to an established and loyal customer base of banks and an association with their trustworthy reputation.

Advantages and Trade-offs

A bank-fintech collaboration will be successful if they use each other’s competitive advantage to compensate for their own flaws. For example:

- Cost-effective and faster implementation of technology

Many traditional banks experience ‘analysis paralysis’ when deciding whether to buy or build technologies. Some companies even spend years researching and deliberating on fintech without delivering any benefits to their customers. They can instead take the faster route of licensing with a fintech company and leverage the technology more quickly.

- Long-term focus

In traditional banking, the payback period window for technology investments is extremely short. Some recommend looking for investments with a payback period of less than a year. Banks will have to do away with such short-term ROI horizons. Banks must also use other soft metrics to measure fintech investment ROI.

- Better focus on their core competencies

One advantage of the collaboration is that both fintechs and banks can divert their attention away from non-core business activities. They will have an advantage in concentrating on their core competencies.

- Banks must adapt to taking greater risks

With fewer regulatory constraints, fintech firms can act and adapt to changes faster than their banking counterparts. They are not afraid of taking risks, especially when it comes to lending.

Incumbent banks have compliance, risk, and legal departments breathing down management’s neck when it comes to risky decisions. They need to be flexible and at least willing to accept how fintechs operate.

- Addressing competition from the big techs

In the financial services market, banks and fintech firms face intense competition from big tech firms. These behemoths already have cutting-edge technologies and the added benefit of a massive global customer base. Their advantage poses a greater threat to the fundamental banking mode.

Together, banks and fintech can more effectively compete.

Key Takeaways

After understanding the benefits of a bank-fintech collaboration, the next consideration will be a model for collaboration.

Cooperation between banks and FinTech companies can take many different forms, with the level of financial commitment acting as the cornerstone. Generally, fintech can become a vendor, a tech-service provider, or a referral partner for a bank. In another model of collaboration, fintechs become the lending service providers (LSP) of commercial banks, offering the bank’s digital loans to customers.

The bank-fintech partnership faces numerous challenges, including regulatory and compliance issues, administrative issues, and IT security concerns. However, the benefits of improving efficiencies and providing a broader range of services to customers outweigh those challenges.

Presica provides analytical solutions such as a bank statement analyser, a GST analysis tool, and account aggregator integration.

Our cloud-based products are intended to help with insurance, personal finance, wealth management, and lending decisions.

Interested in learning more about how our tools can assist you?