4 Reasons NBFC Companies Are Succeeding in the Business Loan Landscape of India

Over the last few decades, non-financial banking companies (NBFCs) have become an essential part of the Indian financial system. Despite a lacklustre beginning in the 1960s, currently a significant number of business owners and retailers prefer taking loans from NBFCs over conventional banks.

The arrival of NBFCs has transformed the business loan landscape in India.

The quick loan application process and low-interest rates on loans are some of the major factors behind their immense popularity in recent years.

This article will explore a few other reasons why NBFCs have become increasingly popular in India. In addition, we will also take a look at some of the most notable differences between traditional banks and NBFCs.

How Are NBFCs Different from Traditional Banks?

Although NBFCs and banks have a few overlapping financial functions, there is a stark contrast in the way they operate. One, they are governed by a different set of rules and regulations. While NBFCs comply with the regulations in the Companies Act of 1956, banks are regulated by the Reserve Bank of India (RBI).

There are three main types of NBFCs in India, and they include asset companies, loan companies, and investment companies.

Today, India’s small to medium-sized businesses (SMBs) are turning to NBFCs for loans. Let’s find out why.

How Are NBFCs Changing the Indian Business Loan Landscape?

In this section, we will dive deep to understand why SMBs prefer NBFCs over traditional banks. How are NBFCs different, and where do banks fall short? Continue reading to know more.

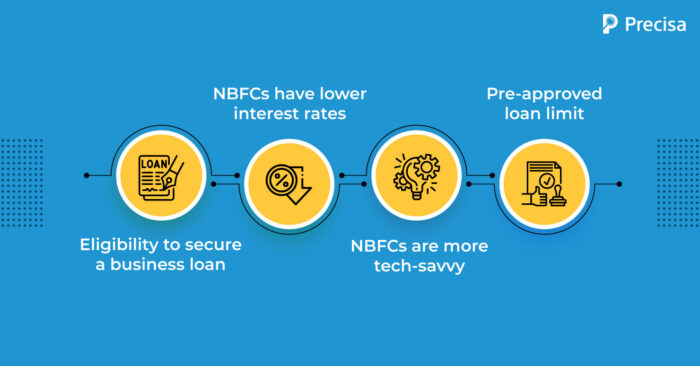

1. Eligibility to Secure a Business Loan

Typically, banks have a strict set of rules and lending criteria. Business owners must collect, organise, and brandish multiple documents and go through a lengthy verification process to secure a loan.

In addition, banks look for higher annual turnover, business experience, and credit rates. All in all, the entire process is time-consuming and tedious.

This is how NBFCs gain an edge. The approval procedure does not involve a series of complicated and lengthy processes. It is a hassle-free approach which primarily focuses on helping customers secure loans without any complicated process. Furthermore, business loans are easily sanctioned even if one has a low credit score and is new to business.

2. NBFCs Have Lower Interest Rates

High-interest rates are putting off, especially for small businesses and startups. Besides, higher interest rates also mean higher easy monthly instalments (EMI). Generally, NBFCs have a lower interest rate compared to traditional banks. This is another reason why small to medium-sized business owners prefer NBFCs over banks.

But have you wondered why NBFCs charge low-interest rates? Interest rates are low as they are defined according to the Prime Lending Rate (PLR), which the RBI does not regulate. Therefore, NBFCs can charge lower interest rates on business loans than banks. NBFCs also have a lower loan processing fee, making them an attractive alternative to traditional banks.

3. NBFCs are More Tech-savvy

We live in the 21st century, which can also be referred to as the digital age. New technologies and innovations are transforming the financial sector in India, and NBFCs are an excellent example of that.

Most NBFCs have embraced the idea of digitalisation to provide a seamless customer experience. Gone are the days when physical documentation and dealing with hard copies were commonly accepted. Today, thanks to digital platforms, it is possible to avail of paperless business loans through NBFCs.

Business owners can secure loans from the comfort of their offices or homes by applying for a loan on the NBFC’s website or by downloading an application on their smartphone. All documents can be uploaded online, and the loan amount is transferred to your bank account within 24 hours after approval.

On the other hand, most banks continue to follow the conventional approach, which requires the borrower to present a paper copy of the documentation and personally check the branch for confirmation. Again, this process is time-consuming, inconvenient, and very counterproductive.

4. Pre-approved Loan Limit

Almost all NBFCs in India offer pre-approved credit-restricted business loans. It is critical to understand that only a certain amount the entrepreneur has withdrawn from the credit line is used to calculate interest and not the whole credit line given to the entrepreneur.

These rules assist companies in maintaining low EMI, which leads to additional savings. Pre-approved credit regulations also enable businesses to reapply for business credit when necessary, mainly if they fall short of funds.

Parting Notes

The Indian lending ecosystem has benefitted from the arrival of modern and new-age NBFCs. NBFCs have transformed the entire Indian lending ecosystem, introducing new lending models that bring the best of both worlds – the modern fintech and the traditional banking sector.

If you are wondering whether NBFCs are the right option, get in touch with our experts at Precisa today.

We have cutting-edge tools to assist automated bank statement scanning tools and important data metrics. We can help you understand the benefits of getting a loan from an NBFC and all the critical aspects of a lending cycle.

Frequently Asked Questions (FAQs) related to NBFCs

1. Are NBFCs better than banks at securing a business loan?

NBFCs are better than banks if you wish to secure a business loan. Some reasons include paperless applications, lower interest rates, swifter loan processing, and better customer experience.

2. Is it safe to take a loan from an NBFC?

Yes, it is safe to take a loan from an NBFC. However, one must do their research and also understand that the RBI does not regulate NBFCs.

3. Is it easier to apply for loans with NBFCs?

Yes, thanks to the relaxed policies and loan processing application, it is comparatively much easier to secure loans with NBFCs.