The Rise of Banking as a Service (BaaS) In India’s Fintech Centre

Banking as a Service (BaaS) has replaced open banking in India, and it is transforming the banking business. This may appear to be a bold statement. However, industry developments such as the rapid expansion of neobanks and the proliferation of customer-centric banking products support it.

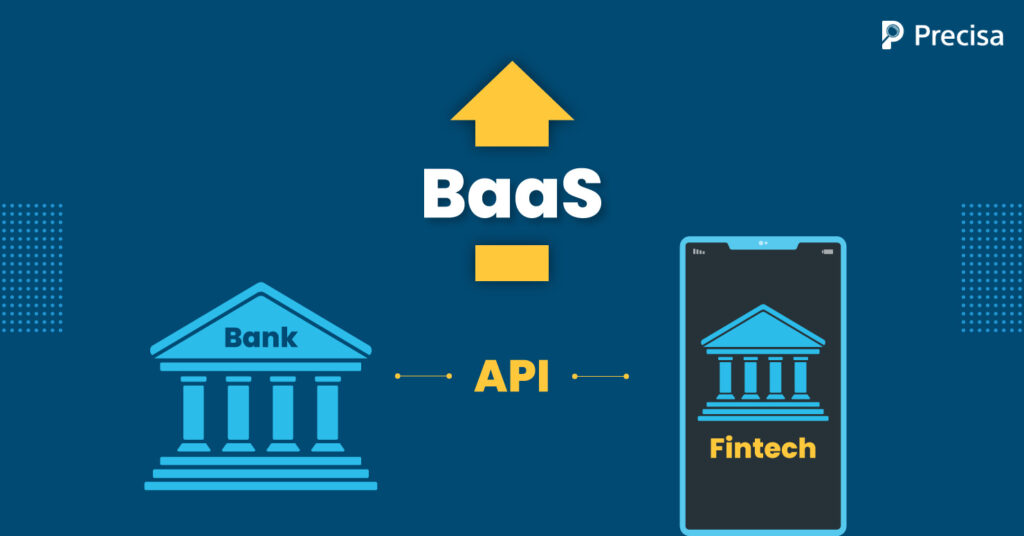

BaaS is becoming more popular as the demand for customer-centric solutions grows. BaaS allows non-bank companies to use APIs to access the banking ecosystem. It has resulted in the reinvention of financial products and services, as well as a shift in the roles of each ecosystem player. Hence, several new players have entered the market.

For insurance companies, neobanks, and other Fintech firms, BaaS has been labelled the “next major transformation frontier.“ It allows them to target a larger number of customers at a reduced cost. Furthermore, by interacting with banks via APIs, non-banks can provide basic financial services to their customers without the hassle of obtaining a bank license.

In 2020, the global Banking-as-a-Service (BaaS) industry was estimated to be worth USD 2.5 billion. By 2031, it is expected to increase at a CAGR of 15.7%, reaching USD 12.2 billion.

Fintechs are eroding incumbent banks’ market share, causing them to experiment with new business models; however, tech-savvy legacy banks may turn this into an opportunity rather than a threat by entering the Banking-as-a-Service (BaaS) space.

As new market players enter, financial inclusion may get a much-needed boost as well. Moreover, it will be interesting to see the innovations heralded by these bank-Fintech partnerships.

What is Banking as a Service (BaaS)?

Banking as a Service (BaaS) refers to Individual products or capabilities developed through the unbundling of banking infrastructure and accessible via APIs to provide specialised banking services (loans, insurance, payments deposits, cards, and so on) in a marketplace model. Fintechs or any other third party running a digital platform can use these APIs and the data they provide to create new and innovative financial solutions that target specific customer needs.

Banking as a Service (BaaS) Transforming Indian Financial Services

With the government’s push to increase support for digital initiatives – INR 200+ crores ($2 billion+) in 2020, in the future, more digital financial products are bound to emerge. This also implies that traditional banks are losing customers to digital competitors despite investing in infrastructure.

BaaS isn’t a brand-new phenomenon brought on by COVID. Its origins may be traced back to 2012, when Credit Agricole, a French bank, opened its app store. In India, RBL Bank and Yes Bank were the first to implement BaaS in 2013 by exposing a plethora of APIs to developers. The State Bank of India has partnered with Uber to provide car financing to drivers; RBL Bank has partnered with Razorpay to provide digital merchant onboarding and payment solutions, and Snapdeal and Freecharge have partnered with Yes Bank to offer immediate refunds.

API offers are currently available from all major private banks in India, including HDFC, ICICI, and Kotak, and many BaaS FinTech startups, such as Zeta, Setu, and Yap, are fast-growing thanks to increased funding. While traditional banks were opening up their APIs, a new wave of Challengers and Neo banks emerged, with digital at the core of their operations.

The advantages of using a Banking as a Service model extend beyond monetising existing infrastructure and expanding customer reach. It all comes down to satisfying the ultimate client need, which involves the use of banking services.

Advantages of Banking as a Service (BaaS)

Traditional banks, by recognising the products and services, can establish non-financial partnerships. Existing banks must adjust their budgets and sales goals accordingly. Banks can take advantage of this burgeoning market to increase revenues and stay competitive if they move quickly.

Indian Banks must utilise BaaS to better serve customer needs. This is only the beginning of embedded finance’s vast potential throughout every customer experience. Customer expectations are rapidly shifting. Banks must think beyond categorising clients into classic, gold, or platinum segments and offer financial services customised to each segment.

Here are some of the advantages of using BaaS, which have helped it become one of the most popular banking trends:

1. Low cost to acquire customers

According to Oliver Wyman’s estimate, the cost of recruiting a customer for a bank is generally higher when banks do not adopt Baas. However, this cost can be lower when using a BaaS technology stack. More importantly, this provides the potential to save up to 95% on customer acquisition costs. As a result, BaaS can help banks and their non-financial partners grow revenues at a fraction of their present costs while also allowing them to take advantage of cross-selling opportunities.

2. Higher customer trust

Traditional banking institutions lost customer trust after the 2008 financial crisis. Customers, particularly the younger generation, have a significantly higher level of trust in technology. The reason for this is that they provide convenience and benefits in real-time. With Fintech making significant inroads into the market, banks may reclaim their consumers’ trust and benefit from BaaS agreements.

3. Access to Innovative Technology

Banks that have been in business for a long time may struggle with low performance since they need to improve their technological knowledge. Meanwhile, they can take advantage of emerging non-financial tech players’ creative technology by utilising BaaS. Banks can use BaaS technology to embed their products onto other platforms rather than investing billions of dollars in digitising their old business methods.

BaaS Future Threats and Opportunities

As the use of Banking as a Service (BaaS) increases, banks will need to focus on preventing commoditisation. Consider a future where there is an open API marketplace with APIs from multiple institutions. End-users will never know which banking API is being used in the backend, so customer loyalty will be formed with the service provider rather than the financial institution that enabled it.

Establishing an open banking API environment is just the start. BaaS products should be adapted to each banking provider’s individual needs. Rather than an API marketplace, banks can provide white label end-to-end financial solutions with data ownership or co-brand the complete solution, as demonstrated with RBL Bajaj-Finserv Credit Cards and TransferWise’s remittance services to multiple neobanks.

BaaS will force banks to rethink where inhouse services are essential and where partner ecosystems may be exploited more than ever before. Additionally, the yearly budget and sales targets will have to be structured in this manner.

Finally, banking executives must incorporate a deeper understanding of technology into their decision-making to build the correct strategy, which is backed by sufficient investment and a partner ecosystem, to leap ahead of the competition. It’s interesting to see how the ancient industry of banking is being reshaped by technology-enabled ecosystems.

The Bottom Line

The impact of BaaS will only increase as the consumer wants, expectations, and technology-enabled capabilities increase. Most banks will need to completely embrace BaaS to stay digitally relevant and maintain market share and industry presence.

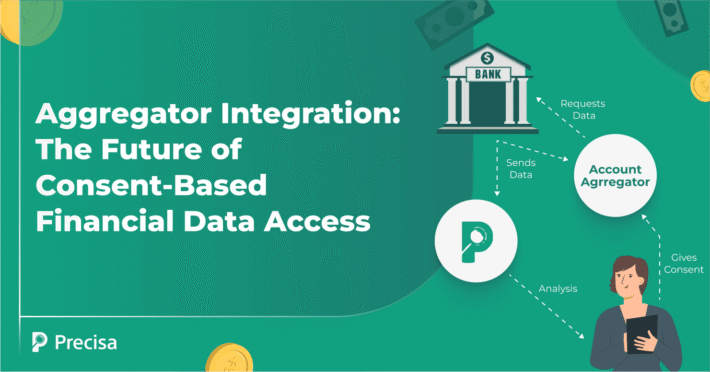

To that effect, Precisa can assist financial players and lenders in improving their lending processes. It helps to streamline loan decision-making and processing at the lender’s end.

Precisa’s bank statement analysis software can cut processing time in half. Using Precisa’s agile bank statement analyser, you can scale your product (loan) at its origin (determining creditworthiness) for the best end-user experience, whether you’re a Fintech or any certified lender. Contact us to know more!