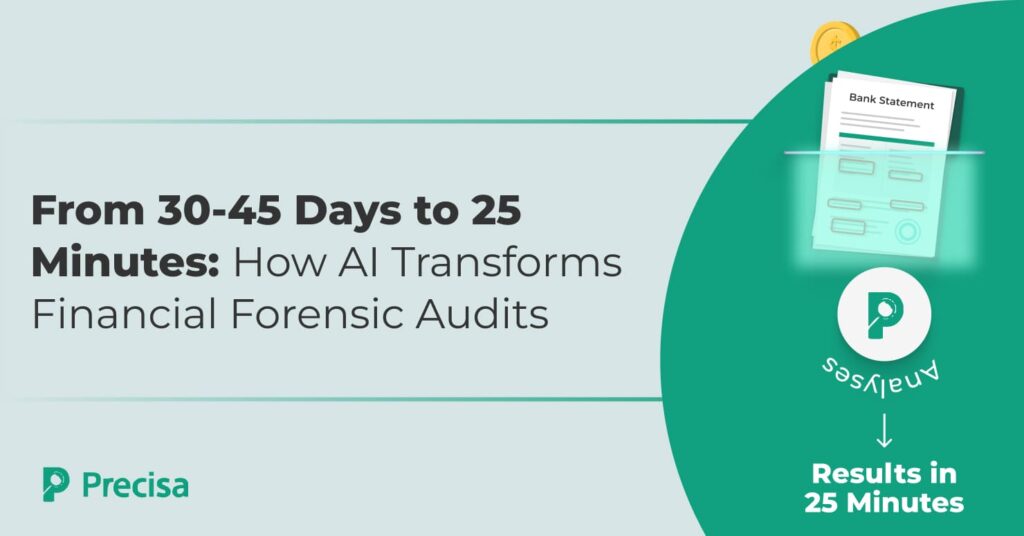

If you’ve ever been part of a financial forensic audits, you know how long and tiring it can be. These audits are essential for spotting fraud, checking creditworthiness, and ensuring compliance. But traditional audits move at a snail’s pace. According to the International Journal of Innovative Science and Research Technology, AI can now perform real-time […]