Identifying the Core Pillars of Open Banking in 2022

In India, open banking has progressed significantly in recent years, and 2021 can be regarded as the year of open banking. Government actions, the launch of scalable Open Banking initiatives by banks, respectable traction by various neobanks, and investment and scaleup of multiple Banking-as-a-Service platforms have all contributed to this movement.

With the rise of Banking-as-a-Service, most well-known and up-and-coming institutions are establishing full-scale BaaS and digital banking departments with clear revenue and customer engagement goals. As a result, there is a noticeable shift in the employment and training of resources for this service.

What is Open Banking?

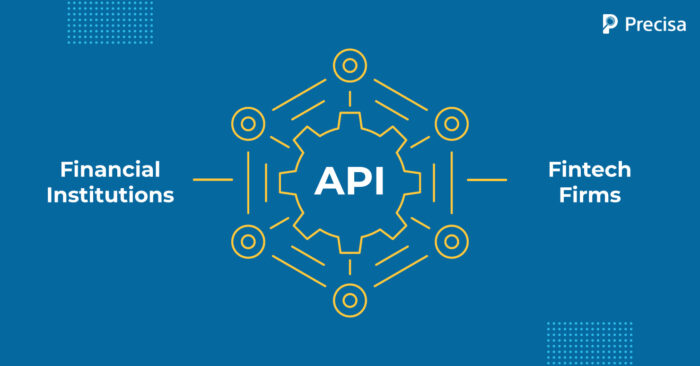

The data generated by financial institutions, such as banks, are exchanged with Fintech firms via application programming interfaces (APIs), which serve as a link between the two, resulting in the concept of open banking.

Open Banking is a system in which data is freely shared with the consent of the customer to develop the necessary analytics and deliver financial and other services. Because permission is a key component of the open banking concept, it is widely assumed that open banking enhances customers’ control over the data they generate.

Indian Open Banking Model

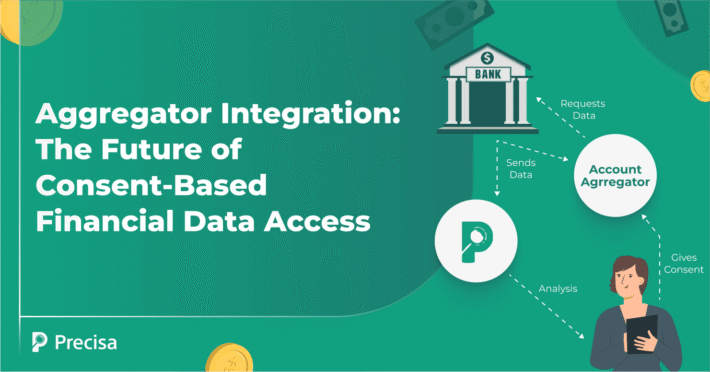

With an active government and market support, the Indian Open Banking ecosystem continues to develop. India has become a global role model for Open Banking Deployments thanks to the emergence of Account Aggregators, API readiness of banks and NBFCs, entry of various neobanks, and heavy investment. Indians already use Open Banking (UPI / AEPS) daily and are likely to adapt to fresh technologies with little difficulty.

Embedded finance models (and neobanks) powered by Open Banking with eCommerce giants, social media companies, mobility leaders, food delivery platforms, Fintechs, and other consumer interaction platforms will account for roughly 40% of the business of digitally savvy banks by 2027. Nearly 30% of firms would use digital platforms (competing with neobanks) such as mobile banking, Internet banking, and Whatsapp banking during this time period.

Core Pillars of Open Banking

Open banking has evolved into six fundamental pillars that each country should adhere to for everyone in the ecosystem to benefit from this global trend.

The following are some of the features of open banking that each government needs to consider while implementing it:

1. Security

The key issues for anybody working in the open banking system are financial privacy and the security of consumers’ finances. Customers’ accounts could be accessed by malicious third-party apps, data breaches could occur, and fraud, hacking, and insider threats are also among the risks.

According to open banking security, customers must be aware of how their data is used, how they can control it, and how it is being stored. Regulations have already been put in place.

One of the most difficult issues that open banking faces is detecting unusual trends in transaction monitoring that indicate illicit behaviour or money laundering. The first step in preventing these crimes is thorough client identification. AI, on the other hand, due to open banking, is capable of far more as it gains a better image of a typical consumer and their transactions.

API access must also adhere to strict guidelines, including technical permission, user authentication, and consent management. As a result, Web Single Sign-on and Identity and Access Management (IAM) must be integrated. All of these add further levels of protection.

2. Control

Open banking regulatory frameworks are structured to allow third parties access to customer-permissioned data while also requiring the third parties to be licenced or authorised and implementing data privacy, disclosure, and consent requirements.

Some frameworks may additionally include restrictions governing whether third parties can share and/or resell data to “fourth parties,” use the data for reasons other than those authorised by the customer, and if banks or other parties can be compensated for data sharing. Expectations or standards for data storage and security may be included in open banking frameworks.

Also, the prerequisites for obtaining a licence should be simple and feasible. This is because ambiguity will lead to unwarranted delays in the licencing procedure, resulting in significant financial investment.

3. Monetisability

The future of Open Banking will depend on the value it offers or the monetisation options it generates.

Participants have the option of bundling or unbundling their offers and services.

The amount of value generated will be determined by a number of factors, including the overall market proposition, customer ownership model, partner value-adds, and risk and liability sharing.

The concept of open banking as a platform can be directly monetized by charging third parties a referral fee for listing and selling products through the banking distribution channel. In some more complicated instances, the third party and the bank may agree to a shared revenue arrangement.

As a platform, open banking initially aids banks in expanding their customer base and offering. Platforms and partnerships will help banks maintain brand relevance and long-term viability in the future.

4. Financial Inclusion

Open Banking is a technology-driven regulatory framework. Consumers who are unable to access conventional banking services may benefit from these Open APIs.

By creating alternate solutions that are more accessible due to the technology involved, open banking has the potential to be the long-awaited solution to financial inclusion.

Through the use of alternative financial data, well designed open banking products can expand access to financial insights that can help consumers get authorised for loans and accurately determine what they can afford.

Open banking is boosting economic growth and promoting financial inclusion by allowing millions of people to transition from cash-based transactions to safe digital financial transactions.

5. Uniformity of Conditions

In the open banking market, big investments can be attracted if it is approached centrally and in line with established standards.

It becomes difficult to access open banking APIs when a TPP has to execute agreements with each bank separately. The requirements of different banks may differ and sometimes contradict one another.

Hence, entering into hundreds of different agreements would be a barrier to market penetration. In a closed market, each bank controls the agreements, which can be terminated at any time at the discretion of the bank.

6. Insurance

Every engaged party must be insured against risks such as fraud, data breaches, and operational disruption to employ open banking features and channels.

To resolve disputes and compensate for possible losses swiftly, each market participant’s liability perimeter should be clearly defined, and a mechanism for resolving developing conflicts and assuring quick damage reimbursement should be established.

In most cases, the cost of insurance is determined by the number of users who have given access to their accounts, as well as the number of payments made by a specific market player in the open banking framework.

Final Thoughts

The purpose of open banking is to address difficulties that were previously addressed inefficiently or not at all. This is an excellent tool for developing a variety of new services targeted to several organisations and use cases, such as eCommerce, accounting, auditing, credit bureaus, finance management, treasury management, and many more.

Open banking, when combined with mobile platforms, allows secure and quick access to financial services from anywhere and in the most convenient format for the user. However, keeping in mind the basics of open banking and responding accordingly is the only way for open banking to work in harmony and benefit everyone equally.

Please keep in mind that open banking is just one of the many ways that the financial sector is changing. Check out Precisa’s bank statement analysis tool to learn how it can make your lending experience much better.