5 Ways to Avoid Falling Prey to Illegal Digital Lending Transactions

As of September 29, 2022, India’s digital lending industry was valued at $200 Billion. The growth of this industry has created more credit opportunities for micro, small and medium enterprises (MSMEs) and other underserved segments. Several legitimate digital lending businesses have contributed to this growth. However, incidents of digital lending fraud are also on the rise.

Eager borrowers are at risk of being duped by unauthorised digital lending platforms. Hence, exercising caution is necessary before parting with sensitive personal information or clicking on links from unusual sources. This blog covers five ways in which prospective borrowers can take precautions to vet digital lending companies carefully before proceeding.

5 Ways to Verify Legitimate Lender

Authenticating and verifying the legitimacy of a lender is paramount to avoid fraud and harassment. Here are five measures you can take to falling prey to illegitimate loan sources:

1. Check If the Lenders Are RBI-Registered

Before choosing a lender, it is important to research the organisation. One important factor is establishing whether the digital lender is registered with the Reserve Bank Of India. The RBI regulates all banks, Non-Banking Financial Companies (NBFCs), and fintechs engaged in digital lending.

According to a circular released on August 10, 2022, all digital lenders must be RBI-Regulated Entities (RE). RBI requires REs to follow specific protocols and rules which protect the borrower from fraudulent practices. For instance, the regulations prohibit digital lending organisations from automatically increasing credit limits without the borrower’s explicit consent.

This regulatory framework also protects the borrower in other ways. For instance, the RE must resolve a complaint lodged by the borrower within 30 days. If not, the borrower can complain to The Reserve Bank – Integrated Ombudsman Scheme. Consumers should visit the RBI website to check if their specific loan app is RBI-registered. The regulator’s website maintains an updated list.

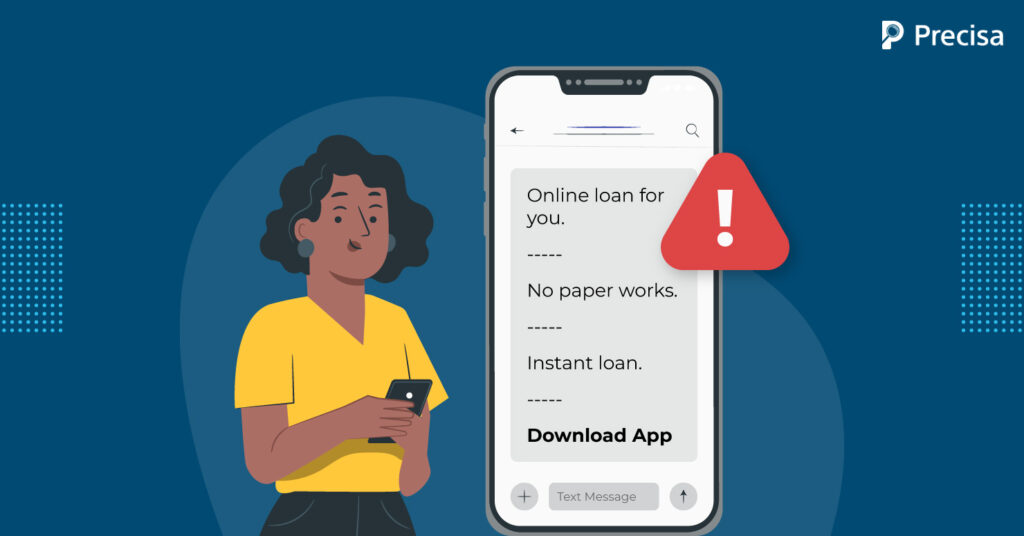

2. Never Click on Unsolicited Links

Consumers may receive a message accompanied by a link containing malware. Clicking on it might compromise one’s device and information. The source of such links is often a professional hacker engaged in phishing with the sole aim of defrauding consumers. The digital lending offer is a disguise to entice a borrower in need.

At times the message and link may appear legitimate. One way to verify it is by emailing the company at its official address. Banks are eager to protect their reputation from hackers and will respond with a clarification. As a general rule, never clicks on a link without authenticating it.

3. Don’t Download Apps Without Due Diligence

A common modus operandi of an unauthorised digital lending platform is that it will ask consumers to download its app. The app will prompt one to share personal information or identity proof.

Never download any app without checking its legitimacy. Moreover, check whether the lender has a partnership with a bank or an NBFC. Never offer additional information such as location or family information.

4. Know the Terms of the Loan

Unauthorised digital lending platforms may entice and dupe consumers with messages that offer credit at attractive interest rates sans documentation. These offers would appeal to those in dire need of credit and cannot secure it from authorised channels, making it easy for companies to defraud consumers.

They can suddenly change the terms and conditions. For instance, the lender might increase the interest rate suddenly, making it challenging for consumers to stick to their payment schedules. The digital lender may harass customers through constant emails and phone calls for payments.

It is crucial to understand the terms and conditions before borrowing. Consumers must know the interest rate, loan tenure, equated monthly installments, and the penalty for late payments. Such information will also help borrowers shop for the best digital lending offer than being driven by panic and fear.

5. Protect Financial Transactions

Many consumers carry out all their financial transactions on their smartphones. Through smartphone usage, one can take a few precautions to protect sensitive data from being compromised. One practice is to ensure that all financial apps are closed after browsing and transactions. Leaving financial apps open can leave one vulnerable to anyone with access to the device. Consumers must ensure that they use complex passwords for finance apps. This is not a foolproof way to protect one’s financial well-being. However, it makes it slightly more difficult to break in.

The Takeaway

The growth of the digital lending industry has created credit opportunities for underserved consumer segments. However, the simultaneous rise of unauthorised digital lending platforms and phishing attacks requires that consumers be cautious when accepting easy loans or clicking on links that seem too good to be true.

It is also advisable for lending institutions to build credibility and trust amongst borrowers.

Poor practices such as hard-selling loans to borrowers with a low credit score without ensuring their ability to repay can lead to the growth of non-performing assets and consumer debt.

Today, several digital lending apps and companies are leveraging automated statement analysis tools to understand a borrower’s credit history and financial patterns before jumping the gun and offering a loan.

Precisa’s automated bank statement analysis tool comes with transparent pricing and customised pricing models to meet the needs of lending platforms. Piqued your interest? Book a free demo today for more information.