The Circular Transaction Trap: How Borrowers Inflate Their Bank Balances?

Do you rely on bank statements to get an accurate picture of the borrower’s financial health, and does the statement you got look perfect? If so, you need to scrutinise the document more carefully to determine whether the statement has been staged. Spotting circular transactions could be a good place to start. Circular transactions involve the repeated movement of funds through multiple accounts, often returning to the original account.

Identifying anomalies, such as circular transactions, offers significant benefits to government agencies in regulatory oversight and fraud detection and helps banks and Non-Banking Financial Corporations (NBFCs) address the NPA burden, which stood at Rs 8,194.83 cr in 2024-25. However, doing this manually is challenging; bank statement analysers are powerful automated tools that provide a real-time and accurate overview of an applicant’s financial health by examining income flows, spending patterns, and cash behaviour.

Find out more about the circular transaction, how borrowers use them to inflate incomes, and what lenders and government agencies can do to deal with it.

Decoding Circular Transactions

Circular transactions are staged transactions, with similar outflow and inflow values, aimed at masking their origin and creating a trail that complicates detection. Borrowers often use these types of transactions, also known as round-tripping, to inflate business activity or income without any genuine exchange of value, making illicit funds appear legitimate.

This can be illustrated with the help of an example: Company ABC transfers funds to a related company XYZ to appear as a legitimate transaction. XYZ shows it as revenue in its statements and later returns the funds to Company ABC, often disguised as a loan repayment or refund. This cycle creates the appearance of healthy cash flow and revenue without any real economic activity.

Although the net financial position of either company remains unchanged, Company XYZ’s financial statements show an artificial increase in revenue or profit for a specific reporting period, which may mislead lenders about its performance.

The convoluted trail, coupled with the large volume of transactions, makes it almost impossible to detect these transactions through manual scrutiny. This is where solutions like Precisa’s Bank Statement Analyser, using cutting-edge technology, offer a solution. Engineered to instantly detect these deceptive patterns, it helps lenders spot red flags, provides a comprehensive view of borrowers’ financial habits, and enables smarter and more inclusive lending decisions.

How Borrowers Inflate Bank Balances Using Circular Transactions?

Borrowers inflate their balances to improve their loan eligibility and qualify for higher loan limits, inflate their turnover to meet lender criteria, and mislead the lender into believing the business is financially stronger than it actually is. Often, money launderers also use round-tripping as one of the techniques to evade detection by auditors and government agencies.

Here are four ways that circular transactions are carried out:

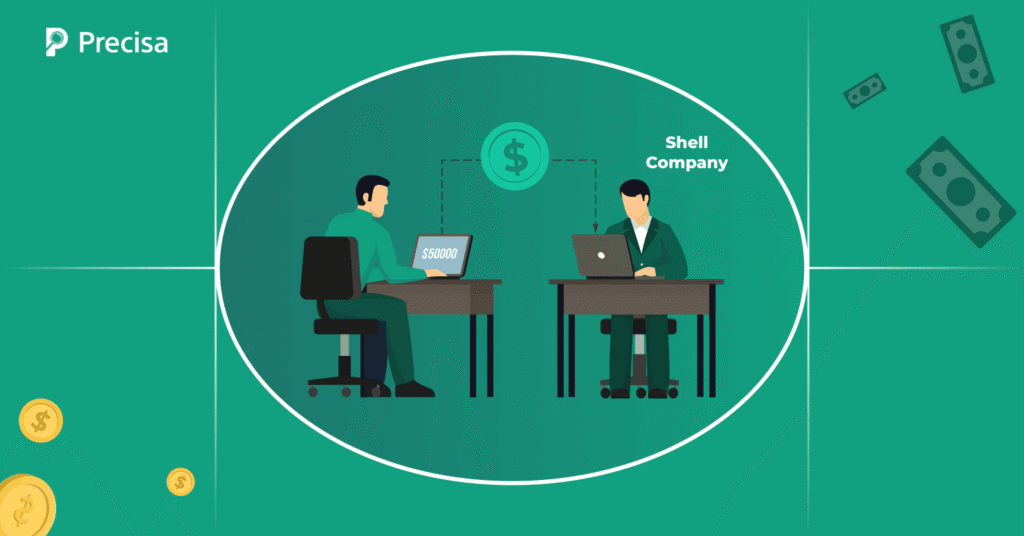

1. Shell Companies

These are entities that exist primarily on paper, without any active business operations or significant assets. Shell companies are often registered in offshore financial centres with lax regulatory oversight. Their real owners hide behind layers of corporate structures, making it difficult to trace the source of funds. Transactions are routed between shell companies to create the appearance of legitimate trade.

2. Asset Transfers

Another way borrowers engage in circular transactions is by transferring assets, such as real estate or securities, between entities at pre-agreed prices to create the illusion of legitimate transactions. While analysing financial statements, lenders and auditors may observe assets bought and sold rapidly at inflated or deflated prices to transfer value without a clear money trail.

3. Loan Agreements

Fake loan agreements between related parties are designed to appear like legitimate financial transactions. Regular “interest” payments are made to provide a pretext for transferring funds, and complex loan structures make it difficult for authorities to detect the true nature of transactions. Loans may be written off without proper documentation, effectively transferring wealth.

4. Fabricated Cash Deposits

Individual borrowers also use circular transactions to inflate their bank balance. A borrower might arrange for a large sum of money to be deposited into their account just before applying for a loan. After the statement period ends, the money is withdrawn.

Precisa’s bank statement analyser helps identify these transactions by flagging same-day credits and debits or credits on bank holidays, which are designed to show a healthy balance and stable income that does not actually exist.

Given the sophistication of these deceptive practices, lenders face a critical challenge: how can they detect circular transactions at scale without dedicating excessive manual resources to statement analysis?

How Lenders Can Prevent and Detect Circular Transactions Fraud?

Detecting circular transactions and other such fraudulent patterns can help NBFCs and banks deal with their growing NPAs, reduce defaults, and prevent fraud. Analysing financial statements provides lenders with valuable insights and helps identify these patterns. However, unlike clearly altered PDFs or entirely fictitious employers, circular transaction traps use real transactions on genuine bank statements, processed through established financial platforms. This makes detecting these patterns exceptionally difficult through traditional tools or methods.

The solution lies in AI-driven software like Precisa’s Bank Statement Analyser that leverages Artificial Intelligence (AI) and Machine Learning (ML) to identify outliers and red flags, such as circular transactions, missing transaction months, or tampered documents. This solution, specifically designed for NBFCs, lenders, and government agencies, automatically scans and categorises large volumes of statements to detect sophisticated patterns that are often easy to miss.

Identifying specific red flags can help identify this type of fraud, but doing so with high-volume statements is difficult. Leveraging technology aids lenders in spotting the below-mentioned patterns, which point towards round-tripping:

- Symmetrical Transactions

Identical or near-identical credit and debit transactions that follow each other closely.

- Identical Counterparties

The same entity name appears frequently as both the source of inflow of funds and the destination of outgoing funds.

- Mismatch of Funds

Inconsistencies between the reported income in financial statements (like tax returns) and the actual cash flow patterns in the bank statements.

- Perfect Statements

A bank statement that appears unnaturally perfect and shows consistent and round-figure transactions can be a warning sign that the data has been manipulated or fabricated.

To Sum It Up

Detecting circular transactions is crucial for maintaining transparency and trust within the financial ecosystem, especially for lenders and government agencies. As borrowers and fraudsters employ increasingly sophisticated methods to inflate their bank balances, it becomes imperative for lenders, NBFCs, and regulatory agencies to adopt advanced technological solutions to help them deal with this challenge.

Leveraging AI-driven tools not only streamlines the due diligence process but also ensures a higher level of accuracy in identifying red flags. The Bank Statement Analyser from Precisa, trusted by 1000+ clients across 25+ countries, is an advanced tool that parses bank statements and clearly tags circular transactions and other anomalies to ensure NBFCs extend credit to deserving applicants only.

Try Precisa’s Bank Statement Analyser for free to see how it detects circular transactions instantly.