A healthy cash flow is the signifier of a thriving business. This financial status is especially beneficial for borrowers who do not own assets, which they can offer as collateral to lenders. Access to cash flow lending is enabling more underserved borrowers to get credit on the basis of business performance.

For lenders, however, authenticating cash flow can be a challenging process. There is a risk of overlooking irregular transactions during the underwriting process.

This is where leveraging cross-analysis tools enables lenders to leverage Goods and Services Tax Returns (GSTR) as a data point and cross-reference it with bank transactions to authenticate the latter.

In this blog post, let’s understand how it works and the role of technology in bringing efficiency and accuracy to the process.

Cash Flow Lending: Explained

Today, a mix of banks, non-banking financial companies (NBFCs) and lending platforms offer loan products. Typically, they have two approaches towards lending. Asset-based lending is a strategy where a borrower can offer an asset as collateral to receive the loan. Assets can include shares, mutual funds, real estate, insurance policies, among others.

On the other hand, cash flow lending is an increasingly popular strategy where a borrower’s creditworthiness for a loan is assessed based on past and future cash flows. It refers to the amount of cash that streams into and out of a business during a pre-determined period. A healthy cash flow indicates that the business is generating sales and revenues, and will be in a position to repay the loan with funds from this pipeline.

However, lenders need a foolproof method to assess the cash flow of potential borrowers. This is where cross-analysing GSTR data with bank account transactions comes into use.

Role of GSTR as a Data Point

Leveraging GSTR as a data point to assess a borrower’s risk profile is a fool-proof method to assess business revenues and, in turn, execute effective cash flow lending decisions.

GST is an indirect, unified tax that the central government levies on selling goods or services. Businesses must file their GST returns (GSRT), i.e., details of every sales invoice raised. Hence, it is a reliable, legitimate data point that indicates actual sales.

Therefore, lenders must cross-analyse GSRT data with the corresponding bank transaction related to purchasing goods or services. But the human eye lacks the speed and efficiency to cross-analyse such data.

Usage of a cloud-based, automated, Artificial intelligence (AI)-powered financial statement analysis tool can accelerate the process and deliver error-free evaluation. This tech-enabled approach enables in-depth comparison of bank transactions and corresponding GSRT data. Wide-ranging cross-analysis is possible in little time.

Borrowers can provide access to bank account statements and GSTR information to lenders. Alternatively, the lender can directly access GSTR information from the Government’s GST portal, with consent from the borrower.

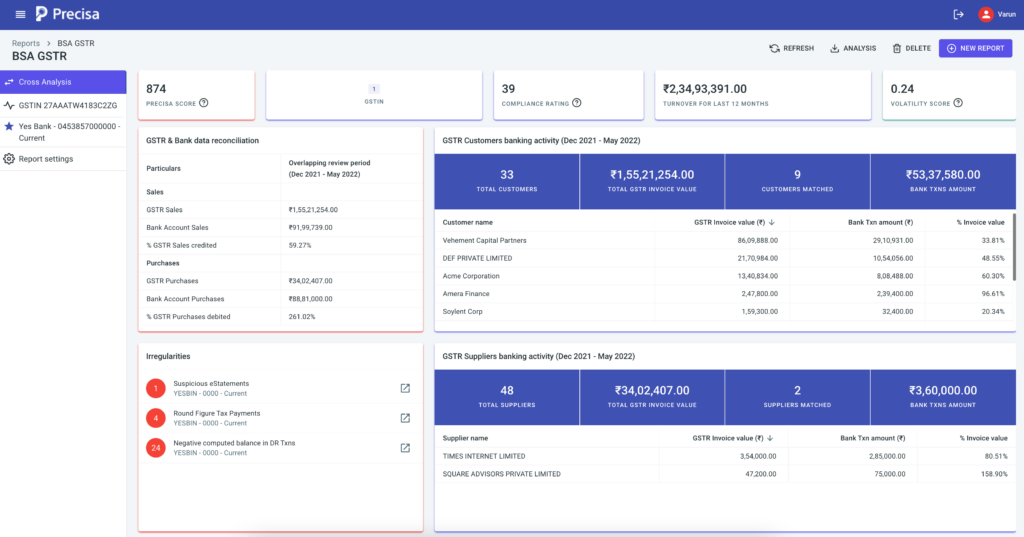

Snapshot of Tech-Enabled Cross Analysis

A bank statement tool, such as Precisa, combines several technologies, such as cloud computing, AI, Machine Learning (ML), and automation, to drive an accurate and efficient cross-analysis process. Here is a snapshot of how it works:

- Lenders can feed in two types of information, separately – bank statements and GSTR statements – and then run individual checks.

- The borrower’s bank statements are automatically segregated into various categories such as revenues, withdrawals, etc, and analysed in detail. A creditworthiness score is generated based on the analysis.

- Lenders can then click on the GST Returns tab, and enter all the GSTR statements. They can either manually add all statements, or pull the data from the GSTR portal after authorisation by the borrower.

- The data is analysed in depth, and a report is generated with an overview of gross turnover, net turnover, and recurring sales.

- Sales data is segregated by state, categories such as B2B, B2C, and exports, by month and year, and customers.

- Lenders can also view a comparison of sales and purchases.

- The GSTR report offers a creditworthiness score based on the data, as well as a compliance score, which reviews how compliant the borrowers are in filing the GST returns.

- The lender can then get the cross-analysis report, a joint report generated using bank statement data and GSTR data. In this report, the latter is cross-referenced with bank statement data, highlighting any discrepancies.

- The cross-analysis report also offers a creditworthiness score, which makes decision-making a data-backed process for lenders.

Benefits of GSTR Cross-analysis

Here are some advantages of the cross-analysis you should consider:

1. Assess the authenticity of sales and revenue

A thorough cross-analysis of bank statement taxation and GSTR data enables lenders to determine the authenticity of sales and revenues effectively.

2. Eliminate circular transactions

Lenders will be able to weed out irregular transaction patterns. For instance, they can identify cases of circular transactions, a scenario where a company sells products to another company and then buys them back. In effect, the valuation of the business does not change. Circular transactions are challenging to track, as multiple companies may be involved. But with the help of cross-analysis tools, they can be easily flagged.

3. Possibility of growth

Lenders will be able to offer cash flow lending to more customers while reducing the risks of loan fraud and NPAs. Thus, they can increase their customer base and capture more market share.

The Takeaway

The rise of non-performing assets (NPA) and loan fraud are the most prominent risks lenders face today. In the Financial Year (FY) 2022 alone, NPA value for public sector banks and private sector banks in India amounted to INR 5.4 trillion and INR 1.8 trillion, respectively.

Therefore, a lending business’s ability to accurately authenticate cash flow will play a role in reducing NPS and loan fraud. In a competitive lending landscape, those who embrace the advantageous use of strategy and technology will have an edge.

Cross-analysis of GSTR data with bank transactions will be critical in accurate, efficient cash flow analysis. Using a cloud-based bank statement analysis solution with cross-analysis capabilities enables end-to-end financial analysis for a spectrum of borrowers. Thus, lenders can ramp up cash flow lending, convert customers, and increase their market share.

Precisa’s comprehensive and seamless financial data analysis solution simplifies and speeds up the process through automation. The software provides actionable insights on a customisable dashboard, thus helping companies make informed business decisions.

Request a free demo today!