NBFC Software: What Lenders Need to Know About Pricing

Investing in NBFC software involves more than selecting the most suitable technology. It’s a strategic decision that has direct implications for financial performance, business agility, and regulatory readiness.

Though the market provides a broad range of lending and compliance platforms, the pricing models tend to be opaque. What might initially look low-cost can rapidly inflate due to phantom charges, paywall features, or costly post-sales support.

In a margin-sensitive and tightly regulated lending environment, underestimating the total cost of ownership (TCO) can compromise profitability, scalability, and compliance readiness.

To avoid this scenario, this article sheds light on the most frequently overlooked hidden costs of the NBFC software.

Why the Real NBFC Software Price Is Often Underestimated

Modern NBFCs increasingly depend on software for loan origination, customer onboarding, underwriting, KYC, and compliance reporting. While software is an enabler of scale, its expense tends to balloon quietly beyond the quoted price.

This is why it happens:

- Base packages rarely include everything. Custom modules, API integrations, advanced analytics, or audit tools are often sold separately.

- Unclear documentation on usage limits results in overages, particularly with high loan volumes or expanding teams.

- Post-sales support and training may be charged on a per-hour or per-user basis.

Even basic operations such as migrating existing borrower data, configuring workflows, or enabling role-based access controls may come with additional charges.

Typical Hidden Charges in NBFC Software

The following are some of the usual hidden fees lenders need to consider in their appraisal process for an NBFC software:

1. Customisation Fees

Custom reports, EMI structures, borrower scoring models, dashboards, etc., that aren’t part of the default offering often attract additional charges.

2. Third-Party Integrations

PAN verification, Aadhaar eKYC, GST validation, and credit bureau pulls are rarely included in base pricing. These critical integrations usually involve additional subscription or pay-per-hit charges.

3. API Access and Transaction Billing

APIs form the foundation of any scalable lending stack. Vendors, however, might limit access, charge per transaction, or offer slow response times unless upgraded to a premium tier.

4. Data Migration and Setup

Migration of the legacy data, like borrower documents, repayment history, and KYC trails, can be done via manual effort, encryption, and mapping. These are usually charged as one-time fees, but can turn out to be costly.

5. Ongoing Training and Support

While initial training may be bundled, refresher sessions, process re-optimisation, or support for new team members often come at a recurring cost.

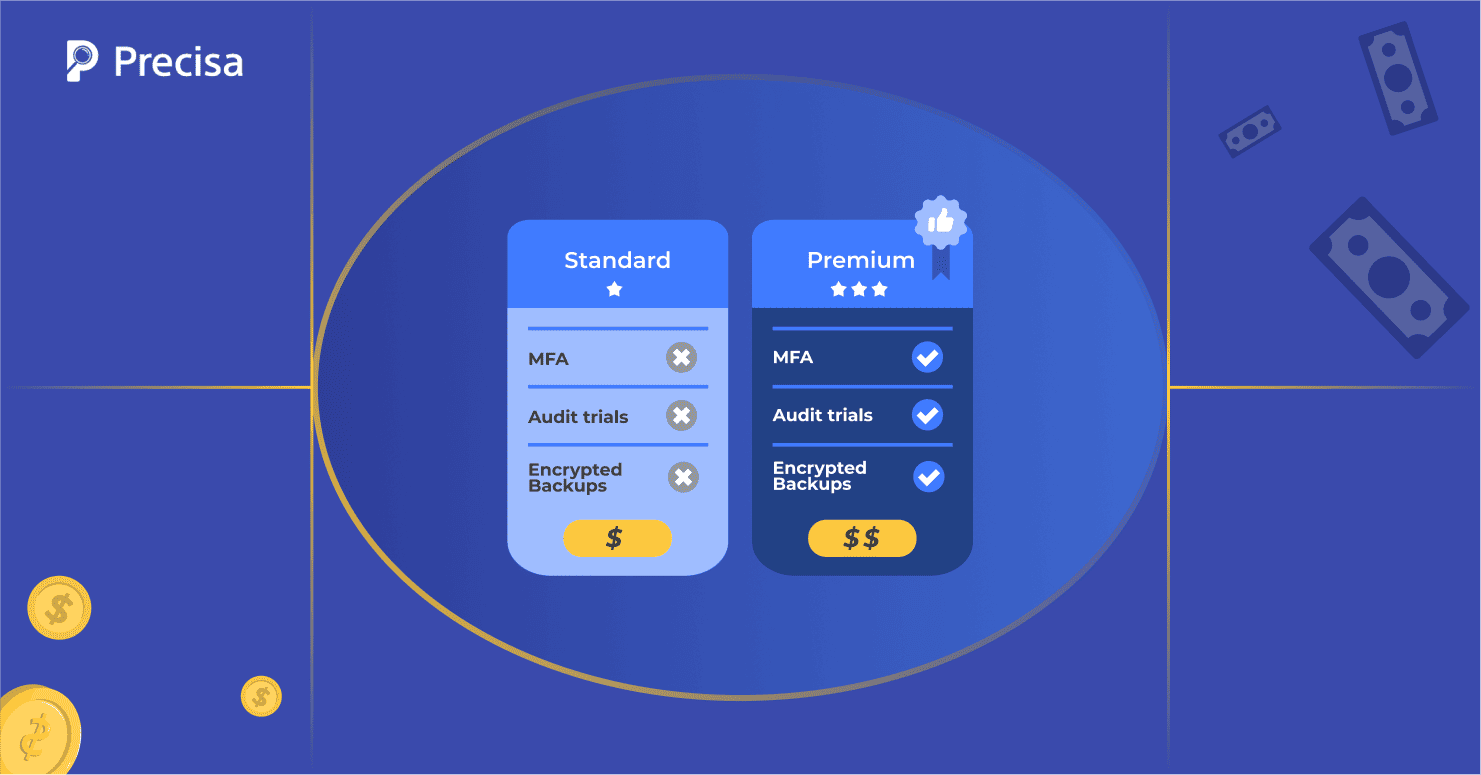

6. Compliance and Security Add-ons

Essential features like real-time audit trails, multi-factor authentication, or encrypted backups are sometimes excluded from standard plans.

It is important to be aware of these possible expenses to prevent budget overruns and secure a clear return on investment.

NBFC Software: The Importance of Transparent Pricing

Transparent pricing fosters trust between software providers and NBFCs. It ensures that all costs are clearly outlined, allowing for better budgeting and financial planning.

Additionally, it demonstrates the provider’s commitment to ethical business practices.

Vendors that prioritise transparent pricing often offer detailed breakdowns of costs, including any potential additional fees, ensuring NBFCs are well-informed before making a purchase decision.

A transparent vendor should clarify:

- What features are part of the base plan, and what counts as add-ons?

- How does pricing scale as your user base or loan book grows?

- Whether implementation, training, and API usage are metered separately?

This level of clarity not only builds credibility but also allows lenders to align software investments with growth strategy, regulatory obligations, and cost-control measures.

NBFC Software: How to Evaluate the True Cost of Ownership (TCO)

Hidden costs often emerge during scaling or in response to evolving regulatory requirements. For example, a platform might impose additional fees for loan volume exceeding certain thresholds or incorporate compliance features, such as audit trails and user access logs.

Lenders need to look beyond quoted price sheets to arrive at what the software will actually cost over time.

A smart evaluation of TCO includes:

- Lifecycle Pricing Analysis: Consider software costs not just for year one but over a 3–5 year horizon, including upgrade cycles and renewals.

- Growth-Proofing Your Stack: Plan for future needs—whether that’s increased API usage, new compliance features, or cross-product expansion.

- Scalability Costs: Will your software scale with your base of borrowers or become cost-prohibitive?

- Downtime and Switching Costs: Evaluate whether vendor lock-in will cost an arm and a leg to switch in the event of performance or support problems.

Ultimately, TCO is where transparent pricing meets operational foresight. An apparently low-cost platform can turn out costly after all the hidden API fees, data migration fees, and support constraints have been summed up.

With the use of transparent pricing alongside strategic TCO considerations, NBFCs can choose solutions providing transparency, continuity, and cost-effectiveness.

Key Takeaway

The selection of NBFC software is a strategic one. Although a low initial quote is attractive, lenders have to weigh the overall cost of ownership, considering data migration, integrations, support, and regulatory compliance.

Vendors who are transparent not only reduce cost surprises but also demonstrate their focus on long-term success.

Precisa delivers a cost-effective and transparent solution to NBFC software with:

- Tiered pricing based on business size and complexity

- Built-in compliance tools aligned with RBI mandates

- Smooth API integrations with credit bureaus, KYC platforms, and PAN/GST databases

- Forensic tracking-friendly data trail maintenance for audit-readiness

Get in touch with Precisa today to learn more.