Why Lenders Should Categorise Bank Transactions (And How To Do It)

Did you know in the fiscal year 2023,

India witnessed a staggering 103 billion digital transactions, amounting to over 166 trillion Indian rupees.

Despite the substantial financial activity across the nation, effectively organising transactions in your bank statement remains a critical task for gaining insights into your spending patterns. Lenders always struggle to figure out if borrowers are handling their money well.

One key tool they rely on is to categorise bank transactions. This means putting all the money you receive and spend into different groups. It helps lenders get what someone’s doing with their money, whether a person or a business.

In this article, let’s delve into why it’s so crucial for lenders to categorise bank transactions and how they can do it better and faster.

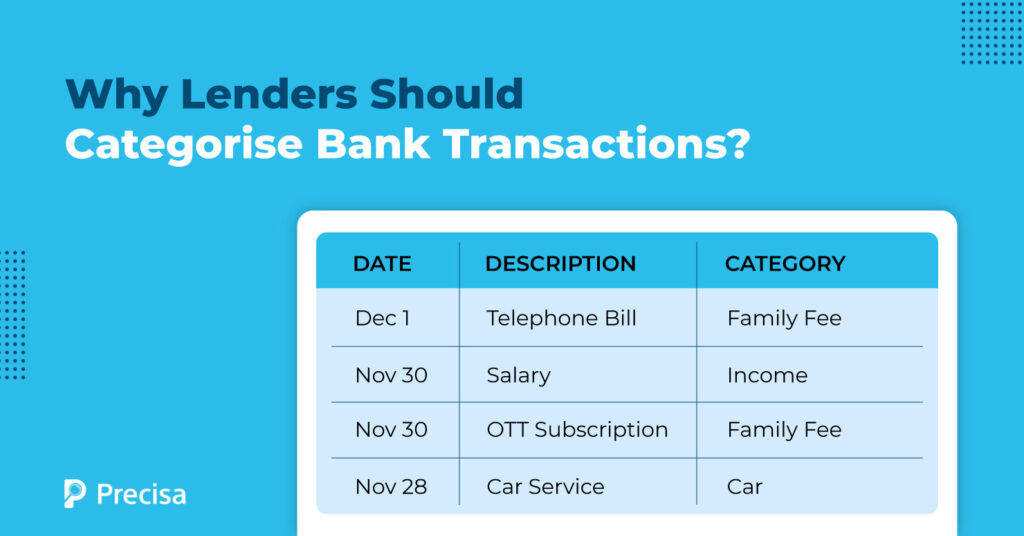

Categorise Bank Transactions: What Does It Mean?

To categorise bank transactions, assigning specific labels or groups to financial activities is required, based on their nature, aiding in the organisation and analysis of expenditures.

This process is vital for effective financial management, budgeting, and accounting. Individuals and businesses assign categories such as groceries, rent, and utilities to transactions, creating a structured overview of income and expenses.

Automation tools or manual reviews can be employed for accurate categorisation. This practice facilitates budget creation, expense tracking, and financial reporting. Moreover, it is crucial for tasks like tax reporting, risk assessment by lenders, and detecting irregularities, contributing to informed decision-making and financial stability.

Why Should Lenders Categorise Bank Transactions?

Here are some key reasons why lenders categorise bank transactions:

1. Risk Assessment

Categorising transactions allows lenders to analyse the spending patterns and financial behaviours of individuals or businesses. This information is crucial in assessing the risk associated with lending money. Certain transaction categories may indicate stability and responsible financial management, while others might signal potential financial stress or risky behaviour.

2. Credit Scoring

Transaction categorisation helps in building more accurate credit scoring models. Lenders can assign different weights to various transaction categories based on their historical correlation with creditworthiness.

A well-categorised history of transactions provides a more comprehensive picture of an individual’s or business’s financial habits, contributing to a more informed credit decision.

3. Fraud Detection

Categorising transactions aids in identifying unusual or suspicious patterns that could indicate fraud. For example, if transactions are suddenly categorised as high-risk or unusual, it might trigger further investigation by the lender.

4. Personalised Offerings

Understanding spending habits and transaction patterns allows lenders to tailor their financial products and services more effectively. They can offer personalised loan products, interest rates, or credit limits based on the individual’s or business’s financial behaviour.

5. Budgeting and Financial Management

Transaction categorisation helps borrowers and lenders alike in budgeting and financial planning. It provides insights into spending habits, allowing individuals and businesses to manage their finances more effectively, which can contribute to better loan performance.

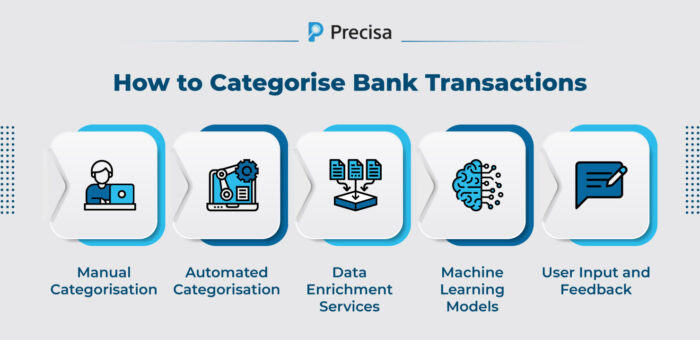

How Lenders Can Categorise Bank Transactions: Key Steps

Lenders can categorise bank transactions through a combination of manual and automated methods. Here are some common approaches:

1. Manual Categorisation

- Transaction Descriptions: Lenders can manually review transaction descriptions banks or financial institutions provide. By examining the narrative details associated with each transaction, they can assign categories based on the nature of the expenditure.

- Receipts and Invoices: Requesting borrowers to submit receipts or invoices for certain transactions can help lenders verify and categorise expenses accurately.

2. Automated Categorisation

- Transaction Categorisation Tools: Various software tools and platforms specialise in automatically categorising bank transactions. These tools often use machine learning algorithms and data models to analyse transaction data and assign categories based on spending patterns.

- API Integration: Lenders can integrate their systems with financial institutions’ APIs to retrieve transaction data directly. API integration allows for real-time access to transaction details, making it easier to automate the categorisation process.

- OCR (Optical Character Recognition): For paper-based receipts or invoices, OCR technology can be employed to extract relevant information and automatically categorise transactions.

3. Data Enrichment Services

Lenders can leverage third-party data enrichment services that provide additional details about transactions. These services can enhance the categorisation process by adding context to transactions that may be unclear based solely on the information provided by the bank.

4. Machine Learning Models

Lenders can develop or utilise machine learning models trained on historical transaction data. These models can learn patterns and relationships between transaction features and assigned categories, improving accuracy over time.

5. User Input and Feedback

Lenders can engage borrowers in the categorisation process by allowing them to manually assign categories to transactions through online interfaces or mobile apps. User input can supplement automated methods and enhance accuracy.

Categorising Bank Transactions: Automated vs Manual Approach

Automated Bank Statement Analysis Tools and Manual Analysis each have their own characteristics. Here’s a comparison of the two:

1. Speed and Efficiency

- Automated: Tools can process large volumes of data quickly, providing instant results. They significantly reduce the time required for data entry, categorisation, and analysis.

- Manual: Manual analysis is time-consuming and prone to human error, especially when dealing with a high volume of transactions.

2. Accuracy

- Automated: Automated tools use algorithms and machine learning to enhance accuracy and consistency in data extraction and categorisation. They are less susceptible to human errors.

- Manual: Manual analysis may involve errors in data entry, categorisation, or interpretation, leading to inaccuracies.

3. Scalability

- Automated: These tools can easily scale to handle a large number of transactions and diverse data sources, making them suitable for businesses with extensive financial activities.

- Manual: Manual analysis becomes increasingly challenging and impractical as the volume of transactions grows.

4. Cost-effectiveness

- Automated: While there might be an initial investment in setting up automated tools, they are generally more cost-effective in the long run due to increased efficiency.

- Manual: Manual analysis can be labour-intensive and costly, especially when dealing with repetitive tasks or large datasets.

5. Complexity Handling

- Automated: Automated tools can handle complex data patterns, anomalies, and contextual analysis using advanced algorithms.

- Manual: Manual analysis may struggle with complex data structures and patterns, leading to oversight or misinterpretation.

Summing Up!

Simplifying lending starts with basic steps like sorting out bank transactions. By using fancy technologies and smart tools, we make sure the data is correct and easy to understand. This helps lenders make good decisions. Automated systems make things easier and prevent mistakes, especially when dealing with confusing transactions. They also keep the data safe from bad stuff.

Sorting transactions is not just a bonus for lenders; it’s a must-have. It puts them ahead in the game of new ideas. Doing this helps lenders decide better, making the financial world more stable. Think about using a smart tool, like Precisa, to give your lending a boost.

It makes it simple for lenders to check transactions automatically, even if they’re written shortly or differently. It looks closely at money coming in (like salary, loans, dividends) and going out (like bills, insurance, spending). This helps lenders check transactions, guess risks, and see what debts are there. Precisa makes things clearer and safer for lenders by using smart sorting. People can pick categories to check closely, like spending each month.

Sing up today to learn more about Precisa.