Decoding Consumer Behaviour: Unraveling Its Impact on Financial Statement Analysis

A customer’s habits play an important role in determining their financial trajectory. For instance, the inability to pay EMIs on time can have an impact on one’s credit score, net worth, assets, and debt.

Access to such vital data related to past customer behaviour can help businesses predict future conduct. In particular, adopting technologies like AI can help businesses predict a borrower’s likelihood of repaying a loan on time, and in full in the future.

This is why, for lenders, in-depth financial statement analysis can be a window into a potential borrower’s past financial engagement. This valuable data can help lenders improve the accuracy of underwriting decisions.

Let us decode customer behaviour and its impact on the results of the financial statement analysis.

What is Financial Statement Analysis?

Financial statement analysis is a process used by lenders to evaluate a potential borrower’s financial health, in the context of their ability to repay a loan.

Thousands of consumers are applying for education, personal, housing, and business loans. Lenders need to make highly accurate decisions to be able to drive a higher Return on Investment (ROI).

This is where automation of the financial analysis process can help lenders decode customer behaviour, comprehensively.

By feeding bank statements, invoices, balance sheets, and alternative financial data into the software, lenders can generate detailed reports that provide insights into customer habits.

How Financial Statement Analysis Decodes Customer Behaviour

Let’s understand how financial statement analysis software tools can shed light on past customer behaviour:

Evaluate all Transactions in Depth

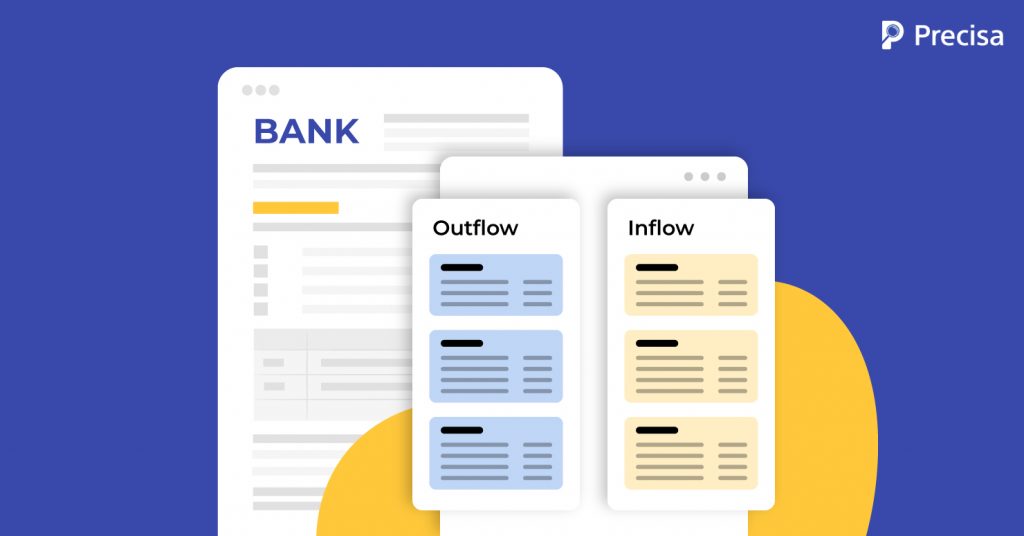

To understand a customer’s habits, it is important for lenders to have an in-depth view of all customer transactions. Bank statements merely display numbers on a spreadsheet.

On the other hand, financial statement analysis software automatically segregates each and every transaction into two main categories – inflow or outflow. Thus every transaction is accounted for.

This approach paints a clearer picture of a customer’s cash flows. Lenders can start building the borrower’s risk profile more accurately based on detailed insights.

Track Spending Patterns

The software segregates every transaction in the outflow category into around 30 sub-categories.

Examples of such categories include employee salaries, customer refunds, vendor payouts, credit card bill payments, fees and charges, EMIs, and taxes, to name a few. The modes of payment, such as credit cards and NEFT to cheques and IMPS are also recorded.

The software generates in-depth reports of a customer’s monthly spending patterns within minutes. These reports paint a holistic picture of a customer’s spending patterns. Any unaccounted transactions are flagged.

Distinguish all Income Sources

Similarly, the software segregates every transaction in the inflow category into around 30 sub-categories.

Examples of such categories include business income, sales revenues, bank interest, capital gains, dividends, and tax refunds, to name a few. In-depth reports of a customer’s income resources can be generated within minutes, which paints a comprehensive picture of all income sources. Again, any unaccounted transactions are flagged.

Spotlight Previous Credit Behaviour

Adopting financial statement analysis enables lenders to understand previous credit behaviour more in-depth via transaction data. For instance, the software can isolate specific outflow transactions that occur due to loan repayment defaults.

These include fees paid due to bounced cheques, late EMI and credit card payments, non-payment, and missing payments due to insufficient funds. A higher number of defaults reflects poor credit repayment behaviour. Hence, there’s a higher potential for borrowers to repeat such behaviour with new loans.

Flag Fraudulent Transactions

Financial statement analysis software, powered by AI, can detect unusual patterns in banking transactions. At times these patterns can expose potential cases of fraudulent transactions.

For instance, borrowers who have engaged in circular transactions can be weeded out. Lenders can generate detailed reports around fraudulent transactions. They can verify the authenticity of transactions and connect the dots to make data-driven underwriting decisions.

Indicate the Debt Service Coverage Ratio

Businesses must have a sufficient amount of liquidity so that they can repay the loans in a timely manner even in the face of market downturns, and other future events. Borrowers who have already taken on extensive amounts of debt can potentially default on future loans unless they have sufficient amounts of liquid capital.

Financial statement analysis solutions can help lenders accurately calculate the debt service coverage ratio. Using this metric, they can predict future credit behaviour.

Gauge Customer Credit Needs

Financial statement analysis software does a comprehensive analysis of all financial data connected to a business. The software also helps lenders evaluate real-time credit needs as well as the ability of a borrower to repay the loan.

Based on various data points, it can recommend customised solutions that are more relevant and affordable for borrowers. This feature is especially useful for businesses that can be classified under the Micro, Small and Medium Enterprises (MSME) sector.

Top 3 Benefits of Financial Statement Analysis

Here’s a round-up of how data on consumer behaviour impacts financial statement analysis and transforms lending operations:

Accurate Assessment of Risk Profile

Financial statement analysis reports offer extensive insights into consumer behaviour. Businesses can make a clear assessment of a borrower’s risk profile based on a mix of key behavioural patterns.

These include credit repayment habits, spending patterns, income sources, liquidity, volume of existing debt, and potentially fraudulent transactions.

Creditworthiness Rating

The software analyses all the available financial data and generates a creditworthiness rating. Sources of financial data comprise bank statements, business balance sheets, Goods and services tax (GST) returns, and credit scores, to name a few.

Loan Customisation

Lenders can automate the process of customising loan products instead of offering standardised products to customers. This approach allows them to serve underserved customers more effectively.

They can capitalise on new market opportunities, accelerate growth for newer verticals, and scale faster.

The Takeaway

Gauging customer behaviour, accurately, can help businesses make data-driven lending decisions, free of biases. The use of AI-powered financial statement analysis software can help lenders make underwriting decisions, quickly and efficiently. It helps them set the terms and conditions of every loan more rationally. They can take on calculated risk and scale, faster.

Presica’s comprehensive and seamless financial data analysis solution simplifies and speeds up the process through automation. The software provides actionable insights on a customisable dashboard, thus helping companies make informed business decisions.

Request a free demo today!