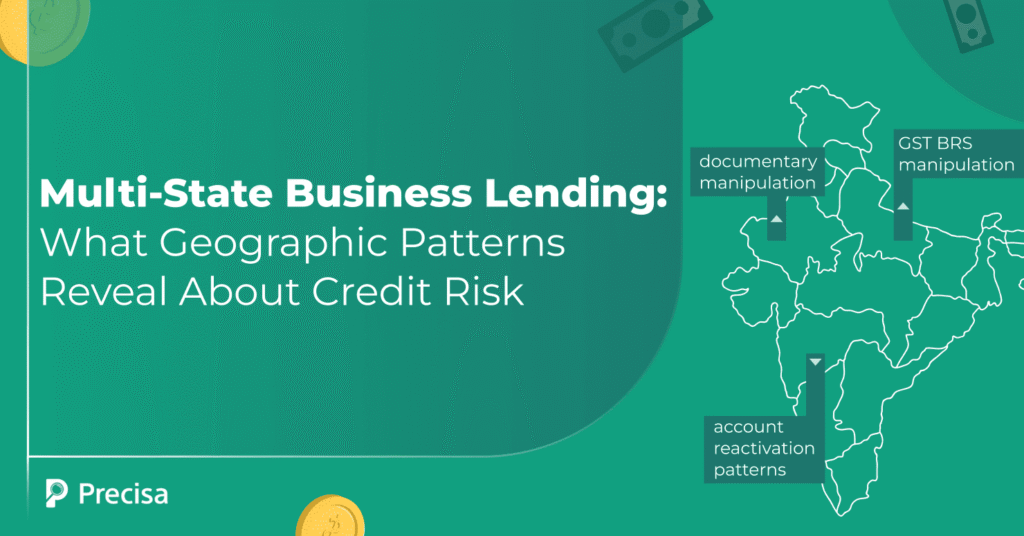

Your underwriter approved a Mumbai trading firm in 48 hours. Clean documents, stable cash flow, CIBIL score of 730. Eight months later, it’s restructured. The Jaipur application you rejected last week? Your competitor funded it, and it’s performing. Same underwriting model. Same credit policies. Different states, different outcomes. India’s ₹46 lakh crore small business credit […]