How Account Aggregators Help with Real-Time Portfolio Monitoring

Customer cash flows change daily. Seasonal swings, gig incomes, and billing cycles make a single financial snapshot unreliable. Quarterly or monthly reviews hide deterioration for weeks or months. By the time you spot a problem, the borrower may already be late.

To manage risk earlier, lenders need visibility that updates as cash flows change. Real-time feeds move monitoring from reactive firefighting to proactive risk management. You can spot income drops as they happen, detect unusual outflows immediately, and intervene days or weeks earlier than before.

That shift matters not just for collections. It affects underwriting decisions, pricing, product design, and customer engagement. An Account Aggregator closes this gap by securely streaming consented, real-time financial data from multiple accounts into a single view.

What Account Aggregators Actually Do

Account Aggregators are RBI-regulated intermediaries that transfer customer-consented financial data from source providers to authorised users such as lenders. Customers provide explicit, time-bound consent, after which the AA securely retrieves authenticated records like bank transactions, balances, GST returns, and investment holdings, and shares only the specific data permitted. Everything is encrypted and auditable, with RBI oversight ensuring clear standards.

Because the data comes straight from the source, you get tamper-proof information, not photocopies, PDFs, or spreadsheets someone might have edited.

Why Real-Time Monitoring Improves Portfolio Health

With continuous monitoring, risk signals surface much earlier. Income volatility shows up as clear rolling trends. Those repeated small outflows you’d miss in a single snapshot? They now reveal emerging cash-runway pressure. These early indicators let you act before stress becomes default, by adjusting exposure, engaging the customer, or repricing the loan.

Once continuous data is available, these advantages become measurable and operational, rather than remaining theoretical.

The Measurable Benefits That Lenders Actually See:

- Faster decisions: Removing manual document collection speeds approvals. Many lenders report 40–50% reductions in origination turnaround.

- Better risk prediction: Continuous inflow and transaction patterns produce richer signals, improving default detection.

- More inclusive lending: Thin-file and small-ticket borrowers can be assessed on real cash flows rather than proxies.

- Lower collection costs: Early intervention increases recovery rates and reduces outreach effort.

These gains are real but only if the data is reliable, fresh and integrated into operational workflows. Precisa’s Bank Statement Analysis combines AA feeds with advanced pattern detection to surface these signals automatically.

How Continuous Monitoring Works in Practice

Continuous monitoring isn’t a single API call. It’s a small data platform that sits between the Account Aggregators (AA) and your core systems. Here’s a concise, practical view of how that works:

- Consent and connect: The borrower grants time-bound consent via the AA consent flow. The system issues and records tokens.

- Secure retrieval: The AA pulls authenticated data from FIPs like bank ledgers, GST returns, investment records, and delivers it to Precisa over secure APIs. All transfers are encrypted and logged.

- Parsing and normalisation: Precisa parses raw transactions, maps fields, and normalises formats (dates, merchant names, GST codes). That makes otherwise messy data usable immediately.

- Event and schedule handling: Data can be pulled on schedule (hourly, daily) or pushed via webhooks when a trigger occurs. This keeps dashboards current to minutes or hours.

- Quality checks & enrichment: Precisa runs validation (missing fields, anomalous balances), enriches transactions with merchant categorisation, and identifies payroll inflows, GST patterns, and recurring deposits.

- Signal generation: The platform converts transactions into underwriting signals (rolling cash-flow, deposit frequency, runway days, abnormal outflow alerts) and publishes them to your underwriting, monitoring, and collections systems.

- Audit and consent trail: Every pull, every consent, and every data slice is auditable for compliance and dispute resolution.

Precisa’s Account Aggregator is pre-built to follow this path. They reduce engineering lift by handling consent logistics, parser logic, and event wiring so your team can focus on rules, thresholds, and collections playbooks.

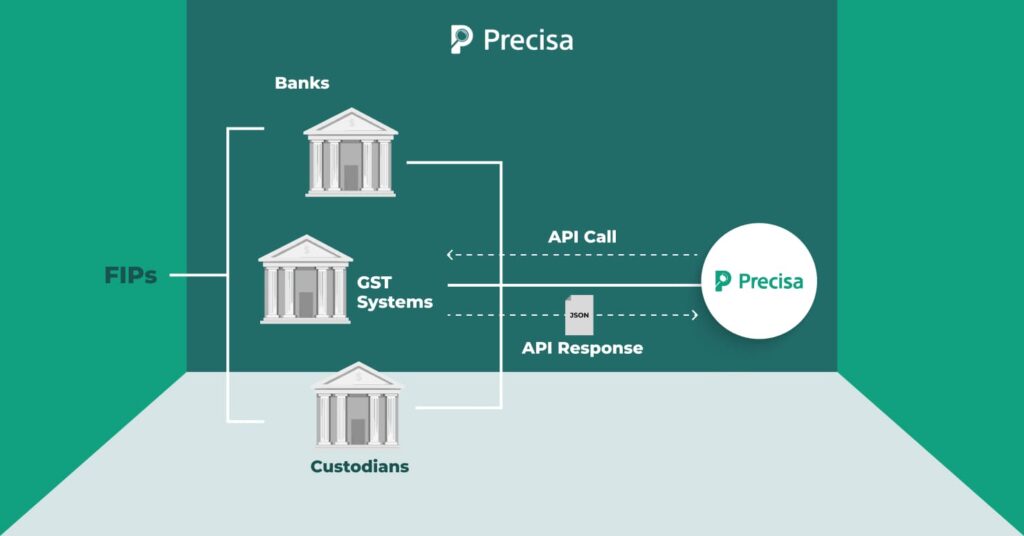

How The AA Data Flow Actually Works

Account Aggregator data flows through a simple, repeatable pipeline that turns raw financial records into usable risk signals.

- Consent & token lifecycle: The borrower grants time-bound consent via the AA consent flow. The AA issues an access token tied to that consent. Tokens expire and can be revoked; your connector must handle refresh cycles and surface consent lapses to ops.

- Data retrieval from FIPs: The AA uses secure, authenticated calls to Financial Information Providers (banks, GST systems, custodians) and fetches authorised records — transactions, balances, GST returns, holdings — typically in JSON or standardised payloads.

- Secure delivery to the connector: Data arrives encrypted (both in transit and at rest) at your connector endpoint. Your implementation should enforce strict access controls and use signed webhooks to verify authenticity.

- Parsing & normalisation: The connector parses raw records, normalises date formats, merchant names, GST, and transaction codes, and deduplicates entries. Normalised fields enable consistent downstream rules and analytics.

- Scheduling and webhooks: Pulls can be scheduled (hourly/daily) or triggered on demand. Implement retry policies and idempotency to handle transient failures. Use webhooks to push fresh data to downstream services in near real time.

- Signal generation & push to downstream systems: Enrichment layers convert transactions into signals: rolling cashflow, payroll detection, abnormal outflow alerts. Signals are published via APIs or message queues to underwriting, EWS, and collections.

- Audit trail & logging: Log every consent, token event, pull, and data slice. Keep timestamped, tamper-proof records for compliance, dispute resolution, and forensic analysis if needed.

A Phased Approach To Plug-And-Play Account Aggregator Connectivity

Account Aggregator connectivity delivers its real value when it moves beyond compliance and becomes operational. But trying to implement everything at once often increases complexity without proving impact. A phased approach lets you prove value fast without overwhelming your tech team or creating operational chaos.

Precisa’s connector is designed specifically for this phased approach. Trusted by 1000+ clients globally, it sits alongside your existing systems rather than requiring core changes. You can pilot with a small portfolio, validate the impact, and scale gradually without major technical debt.

Phase 1 – Pilot

Begin with a pilot. Select a portfolio where real-time signals matter most, such as MSMEs, small personal loans, or merchant lending. Run a representative sample with a narrow, well-defined set of monitoring rules to validate impact.

Phase 2 – Signal Selection

Next, focus on signal selection. Track only the indicators that directly support your credit decisions: rolling deposits, salary inflows, GST turnover, or unusual cash withdrawals. A smaller set of high-quality signals beats trying to monitor everything.

Phase 3 – Operational Integration

Once signals are stable, integrate them into operations. Feed alerts directly into daily workflows so they trigger clear actions, such as prioritised customer outreach, temporary relief offers, or pricing adjustments. Signals should always map to an explicit next step.

Phase 4 – Scale and Refine

Once this foundation is solid, scale and refine. Measure improvements in approval speed, vintage performance, and collections efficiency. Use what you learn to fine-tune thresholds and expand coverage across portfolios.

Precisa is built to support this path without requiring major changes to your core systems. The connector runs alongside existing infrastructure rather than inside it, keeping implementation risk, cost, and disruption low.

The KPIs To Track From Day One

Start by tracking metrics that directly connect improved data visibility to financial outcomes.

- Time to decision (origination): % reduction in approval turnaround.

- Consent coverage and data freshness: % loans with valid consent and average refresh cadence.

- Early warning effectiveness: Lead time (days) between alert and delinquency; true-positive ratio of alerts.

- Vintage performance: Default and roll rates by origination cohort.

- Collections efficiency: Cost per account and conversion from outreach to resolution.

These KPIs tie the new visibility straight back to balance-sheet outcomes.

Final Thoughts

Account Aggregators turn intermittent financial inputs into continuous, auditable signals. For NBFCs and lenders, this leads to fewer surprises, more accurate pricing, and earlier intervention when risk begins to build.

When implemented effectively, continuous monitoring becomes a core risk control rather than an optional add-on. If you would like to see how this works on your own portfolio, you can try Precisa risk-free with a free trial.

Validate the impact before you scale. Try Precisa for free and monitor cash-flow signals continuously.