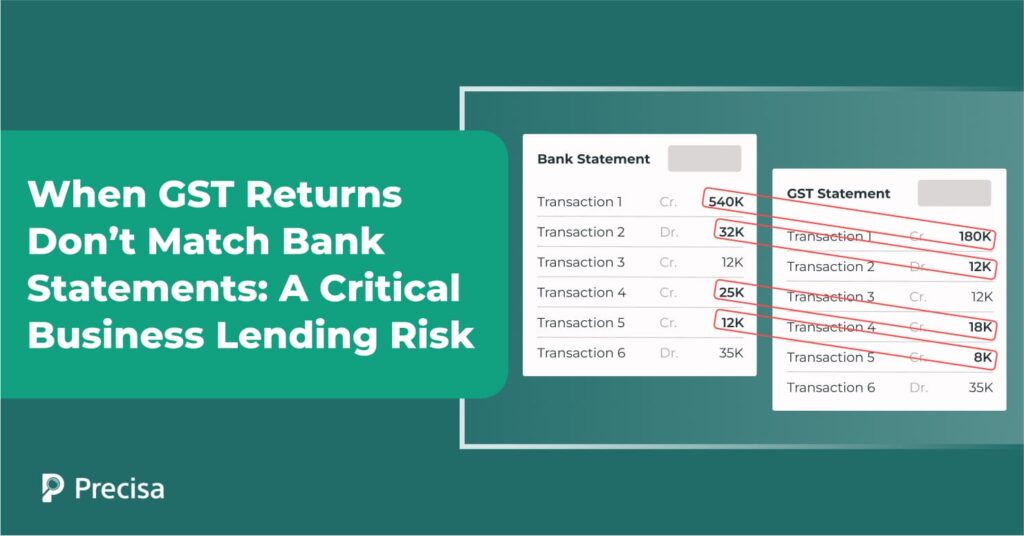

When GST Returns Don’t Match Bank Statements: A Critical Business Lending Risk

GST returns are now one of the most dependable indicators of a business’s financial footprint. They reflect declared revenues, tax compliance, and transaction consistency. However, when GST filings don’t align with actual bank inflows, it raises serious questions about the data credibility and borrower transparency.

According to the CAG report of 2024, the authorities identified over ₹ 2,203.57 crore in mismatched and inconsistent GST claims last year—highlighting how pervasive this issue is.

For lenders, these discrepancies go beyond accounting errors; they directly affect credit risk assessment, portfolio health, and compliance integrity.

This article explores what causes such mismatches, why they present a real risk in business lending, and how data intelligence and automation can bridge the gap between declared and actual financial activity.

Why GST–Bank Statement Mismatches Happen

In business lending, the accuracy of financial representation is non-negotiable. GST filings show what a business reports to the government, while bank statements show what truly happens on the ground.

When the two diverge, it exposes cracks that can carry significant risk in business lending.

It usually occurs because of:

1. Revenue Inflation or Underreporting

Declared sales in GST returns that do not match actual deposits often indicate inflated invoices or undisclosed income. This can distort repayment capacity models and mislead credit evaluation.

2. Unrecorded Cash Transactions

Businesses frequently conduct partial or full cash sales that never make it into the GST system. While not always fraudulent, they create opacity in revenue visibility and weakens cash flow predictability.

3. Timing and Reporting Gaps

Sometimes mismatches happen due to delays—payments reflected in bank statements after GST filing periods, or invoices booked but not yet received.

While some timing differences are benign, recurring gaps are an indication of weak reconciliation practices that may conceal underlying liquidity stress.

4. Fraud and Fictitious Invoicing

Inflated input tax credits and fabricated invoices represent common fraud tactics to secure higher working capital limits. When this happens, bank statements act as a reality check—revealing when claimed credits or sales lack corresponding deposits, signalling possible misrepresentation.

5. Manual or Data Entry Errors

Though GST filings are now digital, reconciliation remains largely manual. Small errors in data entry, invoice mapping, or omission can introduce a 1–4% error rate—eventually widening the gap between reported turnover and actual bank inflows.

The Broader Business Lending Implications of The Mismatch

The implications of mismatched data go far beyond operational inconvenience, directly affecting the credit quality of decisions and a lender’s portfolio stability.

Compromised Credit Assessment

Reliance on unverified GST data can skew a borrower’s actual earning capacity. Lenders can approve large loan amounts based on exaggerated turnover or overestimate working capital requirements, resulting in credit mispricing and future defaults.

Portfolio Vulnerability and NPA Risk

Data mismatches that go unnoticed during credit assessment compromise the integrity of the entire portfolio. The result is inflated loan exposure, delayed stress recognition, and a higher probability of non-performing assets.

Regulatory and Audit Exposure

Inconsistent GST–bank alignment raises red flags during audits and supervisory reviews. Data-backed due diligence is mandatory. Missing reconciliations also increase the likelihood of RBI scrutiny or penalties.

Operational Inefficiency

Manual reconciliation of GST returns and bank data slows approval cycles significantly. For high-volume business lenders, this creates an operational bottleneck that restricts throughput and raises acquisition costs per loan.

In essence, what appears as a minor data mismatch compounds into strategic risk, affecting not only loan-level accuracy but the overall health and compliance posture of the lending institution.

How Data Intelligence Resolves the Mismatch Challenge

PwC India’s 2025 report reveals that automation and agentic AI are transforming financial services operations—driving near-zero invoice reconciliation errors, cutting manual touchpoints by up to 70%, and reducing follow-ups by nearly 60% across vendor and review workflows.

Here’s how modern business lending workflows are addressing the GST-bank data mismatch concerns:

1. Automated Reconciliation at Scale

AI-driven systems parse data from GST filings and bank statements simultaneously, matching each transaction to identify discrepancies. This eliminates repetitive manual work, improves data accuracy, and shortens review cycles that once took hours.

2. Transaction Categorisation and Pattern Recognition

Machine learning models analyse spending, deposits, and transaction patterns to identify unusual inflows or round-tripping. Such granular insights reveal if the business’s claimed activity aligns with actual financial behaviour.

3. Real-Time Compliance Validation

Modern systems perform real-time compliance validation, correlating declared liabilities and filing timelines with actual tax payments to ensure data consistency and authenticity.

Automated audit trails keep lenders inspection-ready at all times, minimising the risk of regulatory non-compliance.

4. Unified Financial Visibility

A consolidated dashboard allows risk teams to view both GST returns and bank data on one screen, highlighting mismatches, trends, and potential business lending risk zones. This single-source visibility simplifies underwriting and periodic portfolio reviews.

Key Takeaway

When GST returns don’t align with bank statements, the integrity of the business assessment comes into question. These mismatches distort risk evaluation, slow decision-making, and increase exposure across every layer of the lending process.

Using AI-driven reconciliation and transaction categorisation, lenders can shift from reactive to predictive risk management—spotting inconsistencies before they evolve into defaults.

Precisa powers this transformation at scale with its GSTR Analyser, delivering:

- AI-powered anomaly detection for automated GST–bank reconciliation

- Real-time validation of business turnover and cash flow health

- Configurable compliance checks meeting RBI and KYC requirements

- Unified dashboards for streamlined audit trails and portfolio insights

By bringing this precision into the business lending workflow, Precisa empowers institutions to lend faster, smarter, and with greater confidence.

Contact us today to discover how you can transform mismatched data into reliable credit intelligence with Precisa.